Booming Market, Thriving Business: TDW’s Rise in Zimbabwean Real Estate

This is a company you need to watch.

TDW is shaking up Zimbabwe's property industry with millions in USD revenue, over 70% annual growth, and hundreds of homes built.

Let's unpack, the property industry, why TDW is growing so fast and the company's potential and risks.

Troika Design Workshop (TDW) is an architectural design studio that also owns a property development business called Turnbury Property Developers. The company was founded in 2015 and is run by a team of young professionals with an average age of 33.

TDW is a private company, but they provided me financial information and insights on their strategy. Note that this is not a promotional paid post.

I am covering TDW as part of “The Prelist” a list of top, high potential companies that could be listed today or in the near future if they wanted to.

For more background on The Prelist check out the earlier article linked here.

From a revenue side, TDW has grown incredibly fast.

In fact, had TDW been covered, it would have made the Financial Times's fastest-growing companies in Africa based on the current annual growth rate of 76% off a base that was already in the millions of dollars.

What impressive is based on my estimate's TDW is still growing fast and on track to have it's best year in 2024, more than doubling its revenue.

To give you a sense how much revenue they are pulling in, since last year TDW has signed deals worth over $20 million.

This type of growth you usually associate with tech not property.

The driver of this is twofold. Firstly, TDW is an attractive sector.

The property industry in Zimbabwe is on track to grow 20% this year, which is quite strong considering that South African, is expected to grow 4%.

A lot of this growth can be linked to the fact that 55% of all institutional investments are in property. This is a very high %. For context in the United States its about 10%.

So institutions with capital invest mostly in property.

However, it's not just a good market.

TDW has aggressively gained market share by offering a turnkey solution that is attractive to its customers.

TDW, along with its subsidiary Turnbury Property Developers, designs, builds, and even manages a property development on behalf of a customer.

I can see why this all-in-one arrangement may be attractive for large investors who must allocate large amounts of local currency to value-preserving projects.

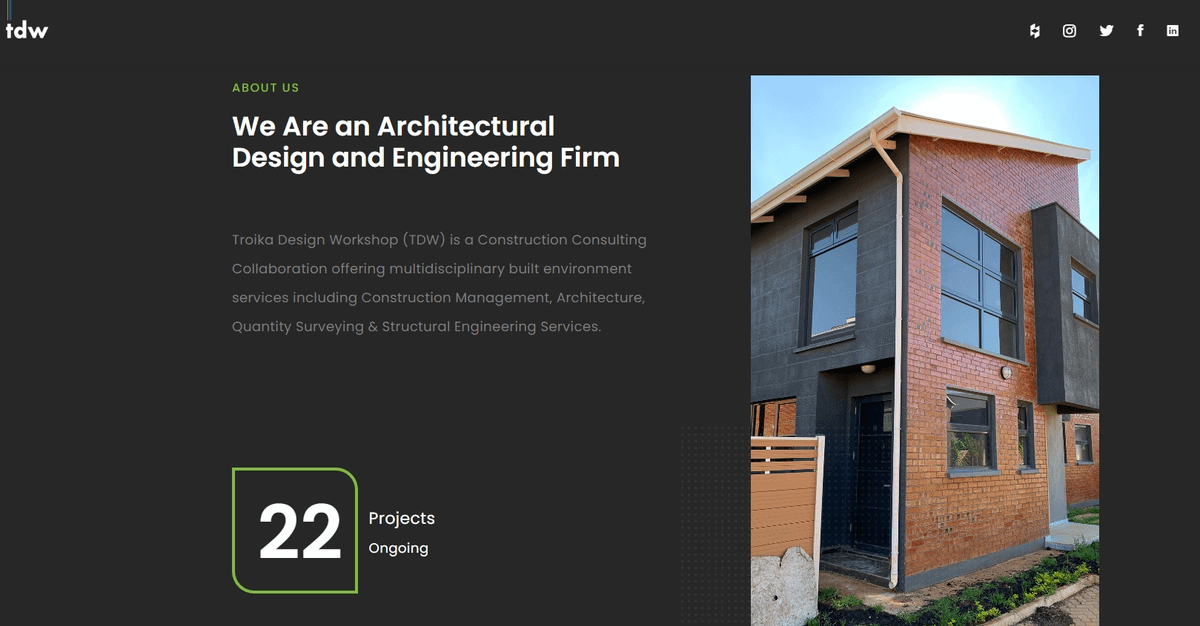

TDW solves that problem. They can take an empty piece of land and turn it into a property like shown below.

The market seems to have responded well to this offering.

TDW has already completed a multimillion dollar project for Stanbic and recently signed another $12millon deal with Old Mutual to build 136 residences and 144 apartment units.

TDW is gaining a lot of momentum, and there are many opportunities that can bring big returns.

However as with all businesses, where there is return, there is risk.

A few risks need are critical for TDW to mange to continue to grow sustainably.

Firstly, the growth in the property market needs to hold. If it collapses TDW could find themselves struggling.

In the short term (2-3 years), I don’t see too much of a slowdown however.

The government has a policy of densification, which means they want more houses to be built in the existing suburbs. While the government is not TDWs typical customer it does help to be riding on a wave that the government is pushing from a policy perspective.

Another indicator on health of the property market is, the yields in Zimbabwe are still decent at about 8% for residential properties (source Knight Frank report).

Yields have also been higher for newly built modern units like the ones that TDW specializes in although yields may start to come down as more units become available in the market.

What also helps is that rentals for whatever reasons seem to be the most resilient to charging in USD.

To manage the risks of a changes in the rental market, TDW has invested in hiring business analysts who watch market trends.

This is an unusual but probably a smart move. It will be interesting to see if TDW can use these resources to identify opportunities to diversify.

Another risk, which maybe the biggest, is the business model. TDW offers an end to end solution, from design to construction to even leasing the completed property. It also commits to timelines and costs upfront. This is great for the customer but can be risky for TDW.

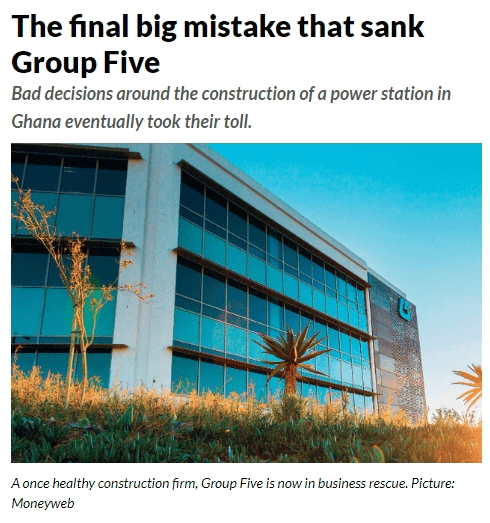

If something big were to go wrong, e.g. construction issues, TDW may be on the hook for a lot costs that may be hard to absorb. An interesting case study that illustrates this is Group Five .

Group Five was a construction giant from South Africa that was valued at over $1 billion in 2007.

Less than 10 years later it was bust with the final death blow being a project in Ghana that overran and ended up costing the company over $60m. TDW can't afford such mistakes.

Another risk TDW probably has a concentrated customer base. This is also just the nature of operating in Zim. For example, TDW's most recent $12m deal with Old Mutual will bring in about $4 million in the next 12-18 months. That is a lot of business from one customer.

These risks are not abnormal but need to be managed diligently as TDW grows. A few things make me a little less nervous about these risks. Firstly, TDW generally seems to be forward thinking.

For example, their financial statements suggest they have focused on investing in the future. In the last three years their aggregate dividend pay out ratio has been about 30%. This means that 70% of profits have been reinvested into the future growth business.

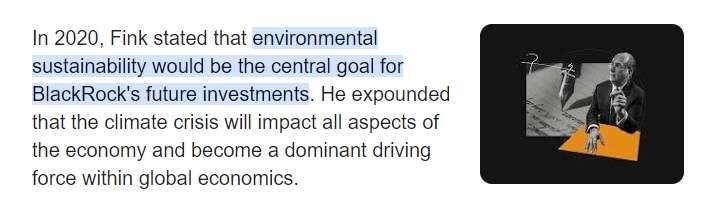

Another example of being forward-looking is that TDW already has an ESG policy, something many companies only have when they become listed.

This is good, not only because ESG is good, but also because it is now increasingly important for investors.

So much so that the CEO of the largest asset manager in the world BlackRock ($10 trillion in assets) made ESG a central part of the companies investment pillars. A strong ESG focus can help in doing good and attracting capital.

All things considered, it seems TDW is in a good position.

If TDW continues to execute and manage its risks while diversifying its customer base, they have the potential to be a listed giant in the region and beyond. If this were a listed stock it should be a buy.

I will be covering TDW on Money & Moves as part of the Prelist, as the need arises.

I would love to get your feedback what do you think about TDW? Thanks for reading!

PS: Since TDW is a private company, there is an increased risk that I am missing something in my analysis. If any verifiable material information arises I will update my analysis as appropriate.

Interesting read. Property market in Zim is experiencing what one would call a boom, wory though is it not an artificial bubble that can burst at any point. On another thought the designation of Harare may not be a big risk to TDW given that land owners in low density suburbs may need their services to develop their cluster homes their constructing on their land.