First Capital Bank Results: A Strong Year, With One Number You Need to Watch

First Capital Bank Zimbabwe just released its full-year results for 2025. The numbers are impressive. Profit after tax hit $30 million, up 52% from $20 million in 2024. Return on equity came in at 33%.

But not all numbers got a perfect score. Alongside the strong operating performance is one area of deterioration that deserves attention.

It does not change the overall picture of a strong year.

It does, however, change the question you should be asking going into 2026.

And it tells you something important about what is happening in the broader Zimbabwean economy.

Let’s unpack!

The Numbers

Let’s start with the headline numbers:

Total income of $84.4 million, up 14% from $74.3 million

Net interest income of $39.7 million, up 20% from $33.1 million

Net fees and commissions of $33.2 million, up 16% from $28.6 million

Profit before tax of $38.7 million, up from $24.9 million

Those are really good numbers across the board, and that Profit Before Tax number is even more impressive, considering that in 2024, $6 million of the bank’s profit came from foreign exchange revaluation gains.

In 2025, that FX gain fell to under $0.5 million, which means the profit in 2025 is driven by operational improvement.

What drove this?

First Capital’s Efficiency: Less Spent, More Earned

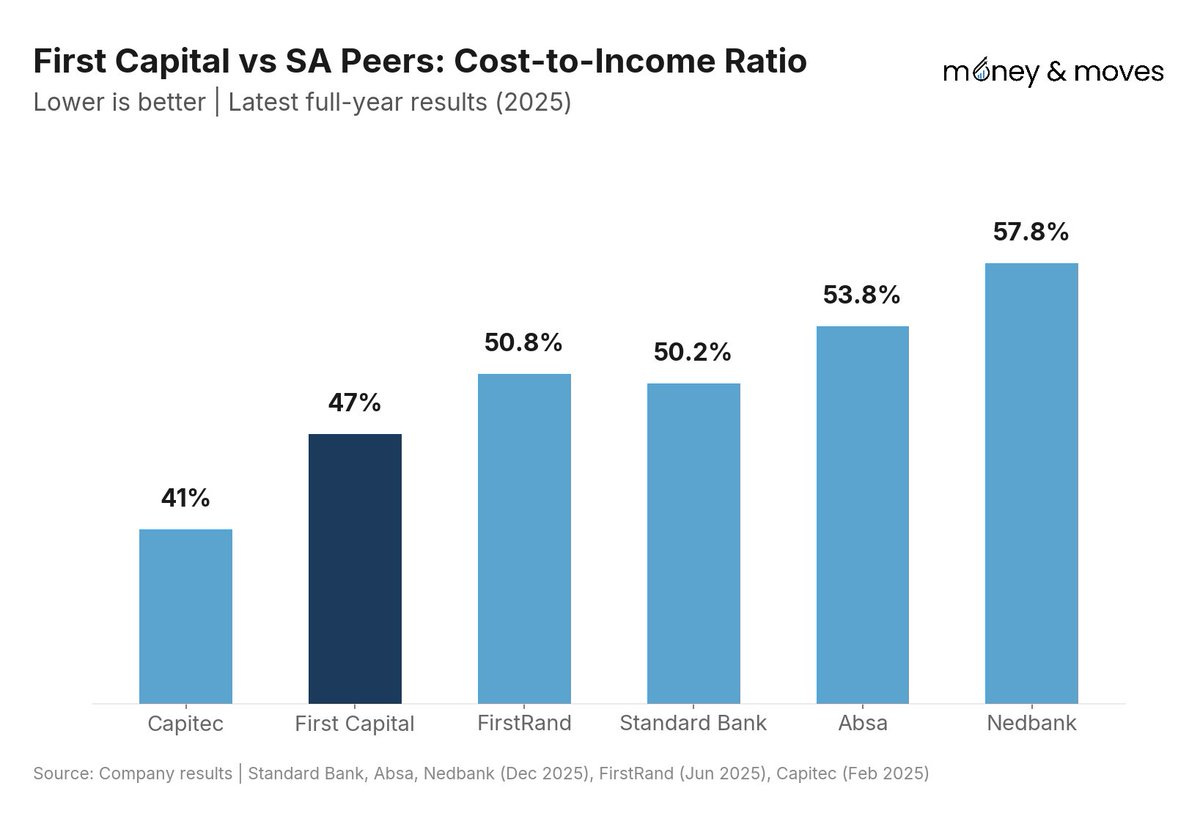

The number that best captures this year’s performance is the Cost-to-Income Ratio (CIR).

The CIR measures how much the bank spends in operating expenses to generate its income.

If the CIR is 63%, it means to make $100, the bank has to spend $63 in expenses. The lower the ratio, the more efficient the bank.

For First Capital, the CIR dropped from 63% in 2024 to 47% in 2025. That is a huge shift in a single year.

Total operating expenses fell from $47.4 million to $43.9 million while revenue grew 14%. Staff costs dropped from $20.3 million to $15.8 million, largely because of retrenchments the bank made in 2024 whose full savings flowed through in 2025.

That last point is interesting.

The bank cut staff, and income went up. That suggests there was a lot of excess headcount that may even have been net negative in terms of contribution to the business.

It raises a question about how many other Zimbabwean banks are carrying a lot of excess staff?

A 47% CIR is impressive for any bank on the continent, as you can see below, even in South Africa, most banks are striving to get under the 50% mark.

Keeping the balance sheet healthy

For a bank, it’s important to make profits, but if your financial health is not strong, profits mean nothing.

For this, we need to look at the balance sheet.

Customer deposits grew 12% to $200 million. The loan book grew 14% to $129 million, funded partly by offshore facilities from Afreximbank and the European Investment Bank.

Capital adequacy sits at 26%, above the regulatory minimum of 12%.

The Liquid Asset Ratio strengthened to 65% from 53%, and the Liquidity Coverage Ratio hit 212%. In plain terms, the bank holds more than twice the liquid assets it would need to cover a stress scenario.

This matters more for a bank than for almost any other type of business. Banks are unique in that a weak balance sheet can cause them to disappear almost overnight.

When depositors lose confidence, they withdraw funds simultaneously, and no amount of profitability can save you from a liquidity crisis. First Capital’s balance sheet does not have that problem right now.

Speaking of weakness, though, there is one number in these results that needs further scrutiny.

The Loan Book: The One Number That Deserves Scrutiny

First Capital’s core business is lending. So a critical part of the operation is making sure the loans they give are paid back.

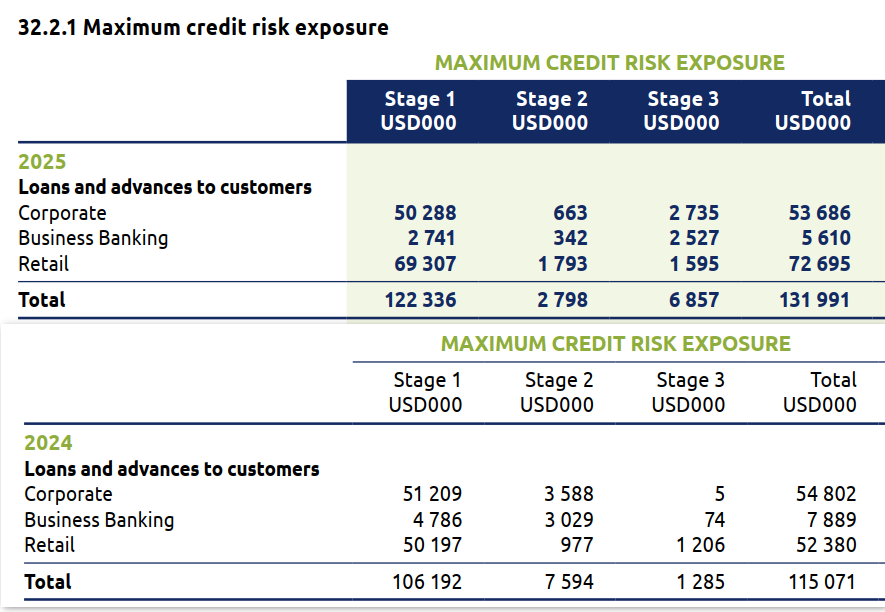

Under Note 32.2 of the results, the bank discloses the quality of its loan book using a three-stage classification required under international accounting standards.

Stage 1 loans are “performing loans” where there is no significant concern. The borrower is current, and the risk of default is low.

Stage 2 loans are where the bank has identified a significant increase in credit risk. The borrower may not be in default yet, but the warning signs are there.

Stage 3 loans are the fully defaulted loans. The borrower is 90 days or more past due, or the bank has concluded that repayment is in serious doubt.

Stage 3 is where you want to pay attention.

Stage 3 loans grew from $1.285 million in 2024 to $6.857 million in 2025. That is a 433% increase in one year. The impairment charge in the income statement jumped from $156k to $3.35 million.

What makes this more concerning is where the defaults are coming from.

In 2024, the Stage 3 problem was almost entirely a retail issue. Individual borrowers, people like you and me.

The corporate and business banking books were essentially good, with Stage 3 exposures of just $5k and $74k, respectively.

By 2025, that picture had completely changed:

Corporate Banking Stage 3: $2.735 million, up from $5k

Business Banking Stage 3: $2.527 million, up from $74k

Retail Stage 3: $1.595 million, up from $1.206 million

The retail book didn’t change much. The jump came from business and corporate lending. That is the more serious problem.

Corporate defaults tend to be larger, more concentrated, and harder to recover from than retail defaults spread across thousands of small borrowers.

The Business Banking situation is the most concerning data point in the entire set of results. Total business banking gross loans sit at just $5.6 million.

Stage 3 exposures within that book are $2.527 million. That means roughly 45% of the entire business banking loan book is now in default.

It also tells you something about the broader economy. SMEs in Zimbabwe are clearly under significant pressure. If nearly half of one bank’s SME business loans are in default, it is a reasonable assumption that other banks are seeing similar stress.

This area of concern doesn’t mean that the business didn’t do well. The impairment charge in the income statement already accounted for most of this; however, it does highlight one risk area that needs attention.

One could argue that the increase in stage 3 loans was just the degrading of loans that had already been flagged last year as stage 2; in other words, the bad loans just got worse rather than fresh issues in the loan book.

There is some data that supports this argument. When there are widespread issues across the entire loan book, you would typically see a gradual pipeline of loans migrating from Stage 1 into Stage 2 before eventually reaching Stage 3.

Instead, Stage 2 loans shrank from $7.6 million to $2.8 million while Stage 3 jumped, suggesting that a handful of borrowers who were already on the watchlist simply tipped into default.

Either way, any time there is an increase in impairment and stage 3 loans, it means there is an increase in credit risk, and credit risk is one thing a bank always needs to pay close attention to.

Overall, First Capital still posted a good set of numbers and has maintained its growth trajectory.

It’s also welcome that a bank is doing well from the core business of lending, which is not the case with most banks that rely on fees and charges.

Where’s the Money? What’s the Move?

At a trailing price-to-earnings ratio of roughly 7x, a 33% return on equity, and a 9% dividend yield, First Capital on paper still looks like a decent investment.

The tricky part is that the share price has already doubled in the last year, and so perhaps has already been rewarded for the strong performance.

But if the bank continues its efficiency gains, grows the deposit base, and manages the loan book stress, there is a case for further upside.

Overall, based on the 2025 results, First Capital looks like one of the better-performing banks in the country right now. The loan book issue is real and worth watching. But it does not, at this stage, undermine what is otherwise a genuinely strong year.

What do you think?

If this was worth your time, it’s worth sharing. Forward it; this may be the analysis that helps someone in your network make an important decision.

P.S. I am working with publicly available information, so I could be wrong or missing something. Thanks for reading!

Good job.

Please do Securities Borrowing and Landing.

Great read! Not sure if i missed it but would want to read more on how OK seems to be collapsing after what appeared to have been a promising would-be turnaround supported by creditors and a decent rights issue.