Not All Formal Retail Is Dying: What Axia's Results Reveal

The key distinction between retailers that are making ground—and what Axia's results indicate about beating informal trade

Over the last few years, formal retail has been associated with struggling businesses.

Metro Peech & Browne and Truworths entered corporate rescue and were effectively sold for $1. Choppies, the Botswana-based retailer, exited the market. OK, Zimbabwe is in distress.

So it’s easy to assume that formal retail is generally a bad business to be in.

However, Axia’s financials prove that it’s not necessarily the case and also serve as a useful case study when it comes to identifying market opportunities.

Let’s unpack.

About Axia

Axia is another “Excor” company—a business that used to be part of the Innscor Group.

It has two main segments: Speciality Retail, made up of TV Sales & Home and Transerv, and Distribution, made up of Distribution Group Africa (DGA), which distributes several brands.

The Numbers

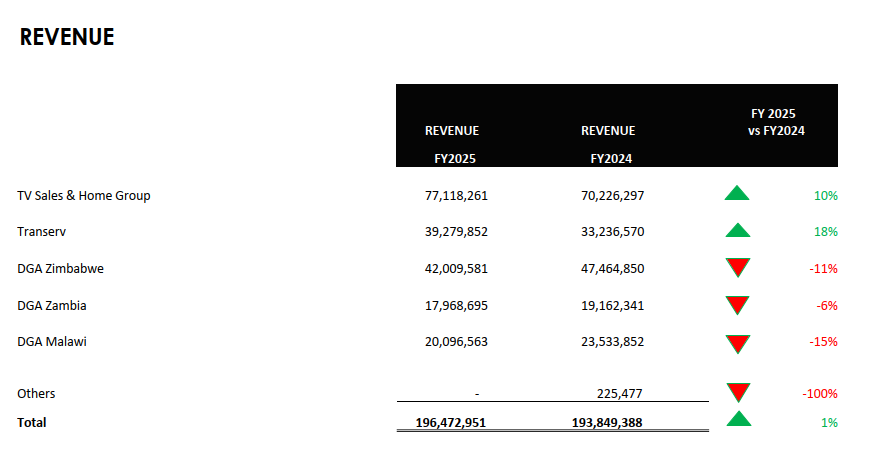

Axia posted solid results for the financial year ended 2025. Revenue for TV Sales & Home was up 10%, and Transerv showed a strong 18% growth.

The drop in revenue in the DGA businesses was not operational but due to an accounting change brought about by restructuring one of its businesses. For DGA Zimbabwe, when you adjust for these accounting changes, revenue actually grew 44%, which is really strong.

Another topic to explore for another day is why distributors like DGA are still performing while formal retailers selling the same goods have been struggling.

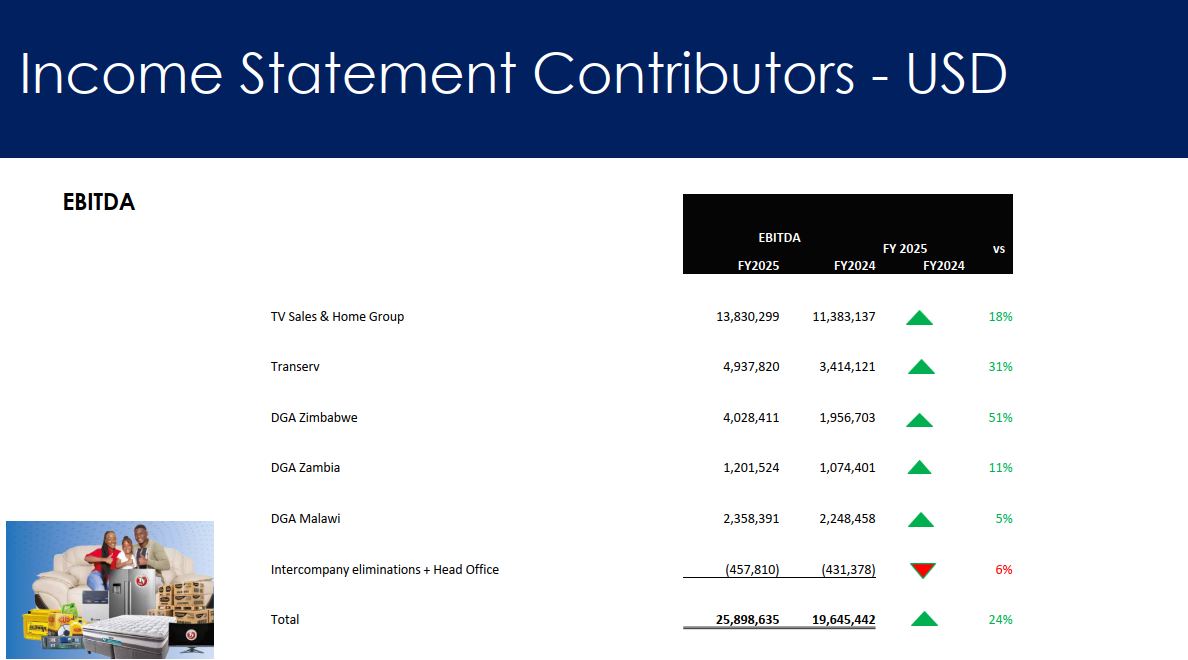

What also improved significantly was the profitability, with EBITDA up 24%.

This makes you wonder: if formal retail is struggling, why did Axia have a strong year?.

Not All Retail is the Same

To understand why Axia is thriving while other formal retailers are struggling, we need to make a simple distinction.

There are two types of retailers: general and speciality.

General retailers sell everyday goods that are standard and well understood by consumers.

Speciality retailers sell products that often need expertise, guidance, and trust, such as car parts, solar systems, and hardware.

Think about it this way: how many questions do customers ask before buying?

For example, when you go buy a Sunlight Dishwashing Liquid at the supermarket, you generally don’t stop a shop attendant and ask several questions about how well it does with plates or spoons or how many washes you can get out of a bottle.

Perhaps in extreme circumstances you may have some questions, but once answered, the next time you most likely just pick up the bottle and put it into your trolley.

Compare this with when you are looking for a spare part for your car or buying a solar system. More likely than not, you will probably have multiple questions and may not even make a purchase decision on the day.

Also the degree of knowlege that the shop attendant demonstrates will likely impact what you buy.

If you ask about how reliable a solar system is, and they say “we don’t really know”. You probably wouldn’t be too keen to make a purchase, and the opposite is likely true.

This distinction is important because when it comes to specialised goods, it is harder for informal retail to disrupt.

For sure, people will still buy car parts from informal traders. However, there is a large segment that will prefer the peace of mind and support during the sales process.

This specialisation is where informal trade is not as strong. Fundamentally, informal retailers’ biggest advantage is pricing; not much is invested in anything else.

As a result, companies that are operating in the speciality retail space have a better chance of keeping customers away from informal retail.

It is worth noting that of late especially with the stability of the ZiG, formal retailers such as Meikles (TM Pick n Pay) are now seeing some signs of growth and recovery.

Where’s the Money? What’s the Move?

In 2025, Axia went under the radar; its stock price only increased by 14% while the rest of the VFEX was up over 60%. Considering the fairly strong performance, there was a case to be made that Axia could have been an attractive investment option.

However, since the beginning of the year, Axia’s stock price has exploded such that between the time when I first started thinking about this article (last week) and today, the share price is up 40%.

While there may be potential for it to rise further, typically the best investments are those where there is a margin of safety.

This basically means there should be a gap between what you think the value of the share is and what price you are paying for it today. It’s basically a buffer, like when you tell your unreliable friend the party starts at 1:30 pm when the real time is 2:00 pm.

With Axia’s 40% increase, that margin of safety has been eaten away. However, stock prices go up and down, so there may be another opportunity to invest in the future.

What the distinction between general and speciality retailers also presents is a strategic option as well. One of the ways to beat out informal retail is if you can specialise in an element of your business, even as a general retailer.

A good example, which we covered last year, was on Food Lovers’ Greendale. By becoming specialists in fresh food, they have been able to avoid disruption from informal retail.

Can other general retailers do likewise?

What do you think?

Thanks for reading. If you found this helpful, please share it with someone in your network and subscribe to the newsletter if you haven’t already done so.

Very informative, even for a layman like myself. Thank you Tinashe.

Good read right here👏🏽…. enjoyed the piece.