Stanbic's Results: Hard to Beat

What the numbers say about Stanbic, the banking sector and the Zimbabwean Economy.

Stanbic Bank just posted one of the strongest sets of results in the Zimbabwean banking sector.

The headline numbers are impressive. But what is more interesting is what these results tell you, not just about Stanbic, but about the Economy and the entire banking sector.

Let’s unpack!

Stanbic’s Year: The Numbers

A note upfront. Comparing 2025 to 2024 income statement figures is not straightforward because the ZWG wasn’t as stable in 2024.

The numbers below are for 2025 only, converted at 1 USD to 27 ZWG. Balance sheet comparisons to 2024 are valid.

Profit after tax: ZWG 1.67 billion ($61.8 million)

Total income: ZWG 4.88 billion ($180.7 million)

Net interest income: ZWG 1.82 billion ($67.6 million)

Operating expenses: ZWG 2.24 billion ($82.9 million)

Total assets: ZWG 35 billion ($1.30 billion), up from $944.6 million in 2024

Loan book (net): ZWG 13.2 billion ($489.7 million), up from $311 million in 2024

Customer deposits: ZWG 20.9 billion ($773.4 million), up from $556.4 million in 2024

Strong numbers across the board. Two ratios bring the real picture into focus.

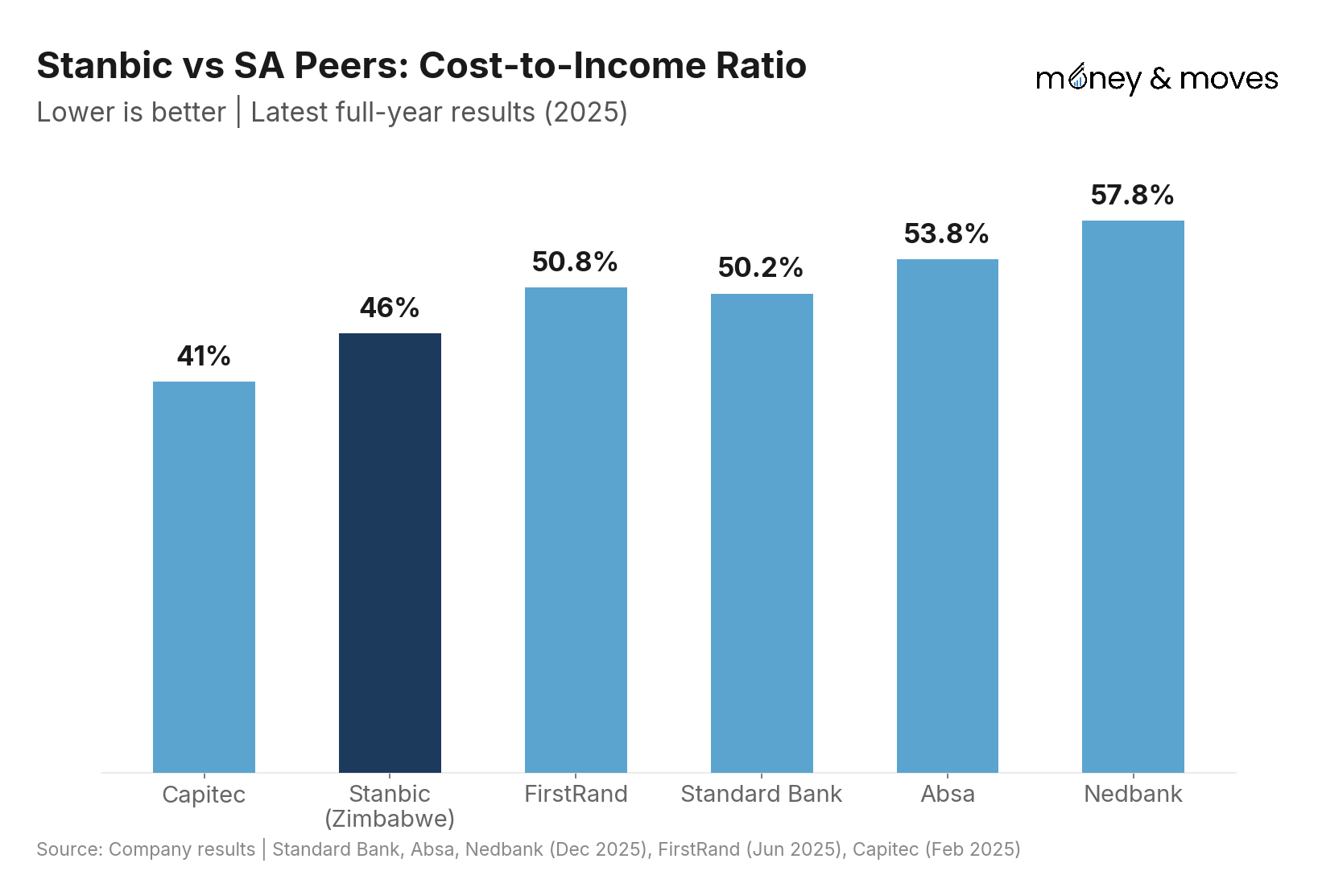

Cost-to-income ratio: 46%. This measures how much it costs a bank to generate a dollar of income.

The lower the number, the more efficiently the bank operates. Below 50% is considered very good. Standard Bank Group, Stanbic’s own parent and one of Africa’s largest banks, is around 50%.

At 46%, Stanbic is doing really well. This is also better than First Capital and much better than most banks in South Africa.

Return on equity: 32%. ROE tells you how much profit a business generates for every dollar shareholders have invested.

Think of it like the return on any investment. If you put $100 into something and earn $32 back in a year, that is a 32% ROE.

Now, a high ROE is not automatically a good thing. Sometimes you get a very high ROE because you are taking a lot of risk.

It’s like that cousin who always has a business idea that can double your money in a week. Technically, if it works, the ROE looks amazing. But the risks involved mean that in the long run, things usually go wrong.

Stanbic does not look like that cousin.

The Bank’s Stage 3 loan ratio, which measures the percentage of loans that are very risk, is just 0.64%. Less than 1 cent in every dollar lent is going bad.

Currently, CBZ Bank sits at 4.9%. First Capital Bank is around 5.2%. There are some reasons for the elevated levels at these banks, but Stanbic is generating a 32% ROE while maintaining a clean loan book and a strong balance sheet, is overall pretty good.

For further context on ROE, Standard Bank Group has an ROE of around 19%. So Stanbic is doing pretty well.

More lending, less fees

Here is an encouraging signal in the numbers. Net interest income, which is what banks make from lending money, grew from 29% of Stanbic’s total income in 2024 to 37% in 2025.

This means more money was made from lending than from fees compared to last year.

This matters for Zimbabwe’s economy. Lending creates economic activity; fees do not and Zimbabwean banks love fees.

The growth in Stanbic’s lending was driven primarily by agriculture, which grew 229% from $32.4 million to $106.8 million. That’s impressive.

Zimbabwe’s record tobacco season probably helped boost that.

But still a lot of fees

Stanbic was arguably the best-performing bank in Zimbabwe based on the 2025 numbers, and while the ratio of Net Interest Income has increased, 63% of its income still comes from non-lending activities, e.g., fees, trading.

In most mature banking markets, the ratio is the opposite. Typically, 60 to 70% of a bank’s income comes from net interest income. Standard Bank Group itself generates around 55% of its income from lending.

The fact that Zimbabwe’s top performer is still well below that benchmark tells you something about the environment. The fees model still dominates because it remains the most reliable way to make money in this market.

Below shows just how bad the split is, with fees and commissions making up 45% of income, even before factoring in FX trading

That is a problem for businesses.

Even if banks do want to lend more, if it's possible to do well from fees, there is less incentive to change the status quo.

There is another number worth paying attention to. Manufacturing loans at Stanbic fell from 32% of the loan book in 2024 to just 10% in 2025.

In dollar terms, that is a drop from $101.9 million to $49.2 million. Does this mean the manufacturing sector is also struggling?

We also saw that in First Capital’s results, their business banking loan book had the most issues. Could this be linked?

Some Interesting News On Property

Stanbic holds ZWG 1.85 billion ($68.7 million) in investment property, representing 34% of total equity.

I have covered this before in two previous articles, “Zim Banks Hold More Property Than SA Giants” and “Property Rich, Capital Poor.”

The short version: Zimbabwean banks hold more investment property than three of South Africa’s biggest banking groups combined, despite being hundreds of times smaller.

What is new here is that Stanbic created a brand new Board Properties Oversight Committee in 2025 to govern this portfolio.

This is interesting.

When a board creates a committee for a specific asset class, it means that the asset has grown large enough to require separate oversight

It will be intresting to see if this portfolio results in any changes in the portfolio.

Perhaps this is the beginning of a more active conversation about whether some of these properties should be unwound to free up capital into the productive economy.

Where’s the Money? What’s the Move?

Stanbic is not listed. You cannot buy shares in it directly. But its results are a useful benchmark to view every bank you can actually invest in.

Banking is one of the most represented sectors on the ZSE and VFEX. On the ZSE, you have CBZ Holdings, FBC Holdings, ZB Financial Holdings, NMBZ Holdings, and TN CyberTech Investments Holdings (TN CyberTech Bank).

On the VFEX, you have First Capital Bank.

Stanbic’s results raise one question every investor or management team in these listed banks should be asking: How efficient is my bank? As Stanbic and First Capital have shown, becoming more efficient can add a significant bump to profitability.

The other thing to look at is the shift from fees to interest income. While fees are the easy money, the growth is in lending.

To grow in this space, however, may require a lot of careful reworking of the balance sheet to meet statutory requirements, keep risk low while growing a loan book.

Let’s see what happens.

Which banks do you think are performing well or falling behind?

Thanks for reading. If you enjoyed this, please forward it to someone you know!

P.S. I am working with publicly available information, so I could be wrong or missing something. Thanks for reading!

Another deeply insightful post and a really useful one too. It has got me thinking seriously about my options in the banking space. First Capital certainly is one option and based on this post Stanbic another. Each will serve vastly different purposes based on the nitty gritties surrounding each account type and how flexible they are on a number of issues and accompanying offers.

Everyone is making money in Zimbabwe,,, or it seems… but i guess i am right check the metal prices and the record profits mining houses will be pocketing this year… Simbisa, Innscor, Delta, Cement is in short supply its like everyone… Im not sure about the techy and telecoms guys but all else seem just ok. I also dont know how im missing it but everyone seems to have found the money making wand.