When Investing in Property Beats the Stock Market (And When It Doesn't)

The Returns of investing in Property's compared to the upside potential from Stocks

If you were investing in the Zimbabwe Stock Exchange (ZSE) before hyperinflation, chances are—you lost money.

In 1999, the ZSE's market capitalisation was $2.4 billion. After hyperinflation, it reopened at just $1.4 billion in 2009.

Through it all, one asset class performed well: property.

The big question is: Has property only outperformed stocks during periods of high inflation, or has it also performed well in a more stable environment?

The “Stable” USD Years

When the Zimbabwean economy dollarised, stocks benefited. The ZSE opened at a low level of $1.4 billion but then rallied, and by the end of 2009, the market capitalisaion of all companies rose to $3.8 billion. In 2010 and 2011, however, values stagnated and remained at about the same level.

This chart from Econet’s 2012 Annual Report also illustrates the same point: a rapid rise in 2009 and a stagnation between 2010 and 2011.

Despite the stock market rebound, Property still seemed to perform fairly well against the Zimbabwean Stock Exchange.

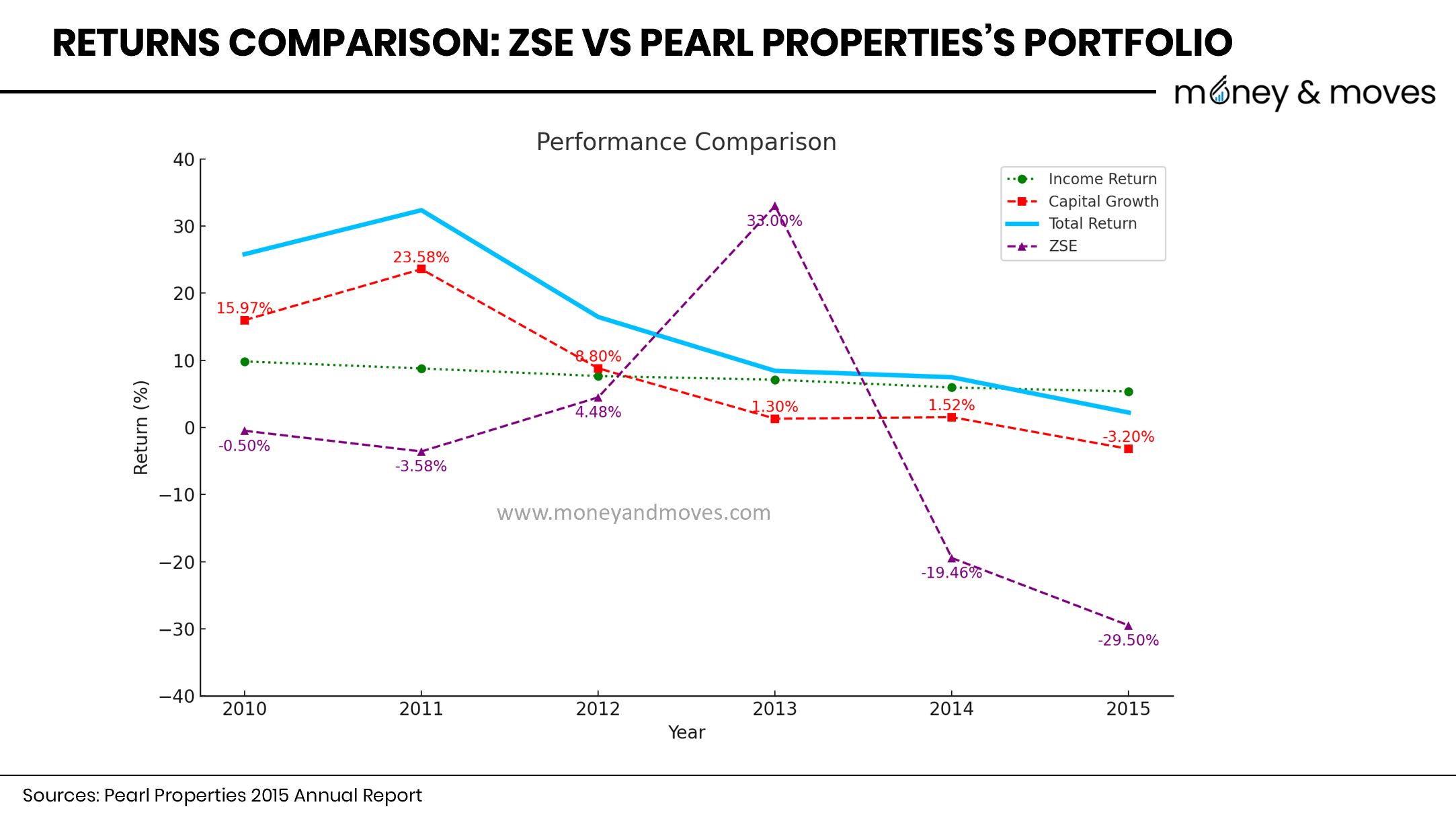

Below is a chart from Pearl Properties’ (now called First Mutual Properties) 2015 Annual Report. This chart compares their property portfolio's returns to the ZSE's returns.

Focus on the red and purple dashed lines, as they offer the closest comparisons. Between 2010 and 2015, Pearl Properties' portfolio (red line) appeared to outperform the ZSE (purple line).

Simply put, $100 invested in 2010 in the ZSE would have been worth $76 at the end of 2015, whereas with their property portfolio, it would have been worth $155.

It's worth noting that this comparison focuses more on one company's commercial property portfolio. However, residential and commercial properties often move in sync, as the same trends typically influence both, and property valuations are often made in reference to the overall market conditions.

Another consideration is that the comparison starts from 2010, which would favour Pearl Properties. If you had been bold enough to invest the $100 in the stock market immediately after dollarisation in 2009, it would have been worth $205 at the end of 2015.

Practically, however, most people wouldn’t have had the USD to invest at that time, and so if you missed the early gains, you probably would have ended up lagging the returns from property.

All this is to say that property generally seems to have held up well in hyperinflation and a more stable USD, low-inflation environment.

Could this be why more people are not investing in the Victoria Falls Stock Exchange (VFEX), despite its offering USD returns and undervalued companies?

Do people believe they can achieve lower-risk returns by investing in property rather than USD-denominated stocks?

Where Stocks Beat Property

While property has generally been quite steady and reliable, one area where stocks have a big advantage is obtaining exceptional returns.

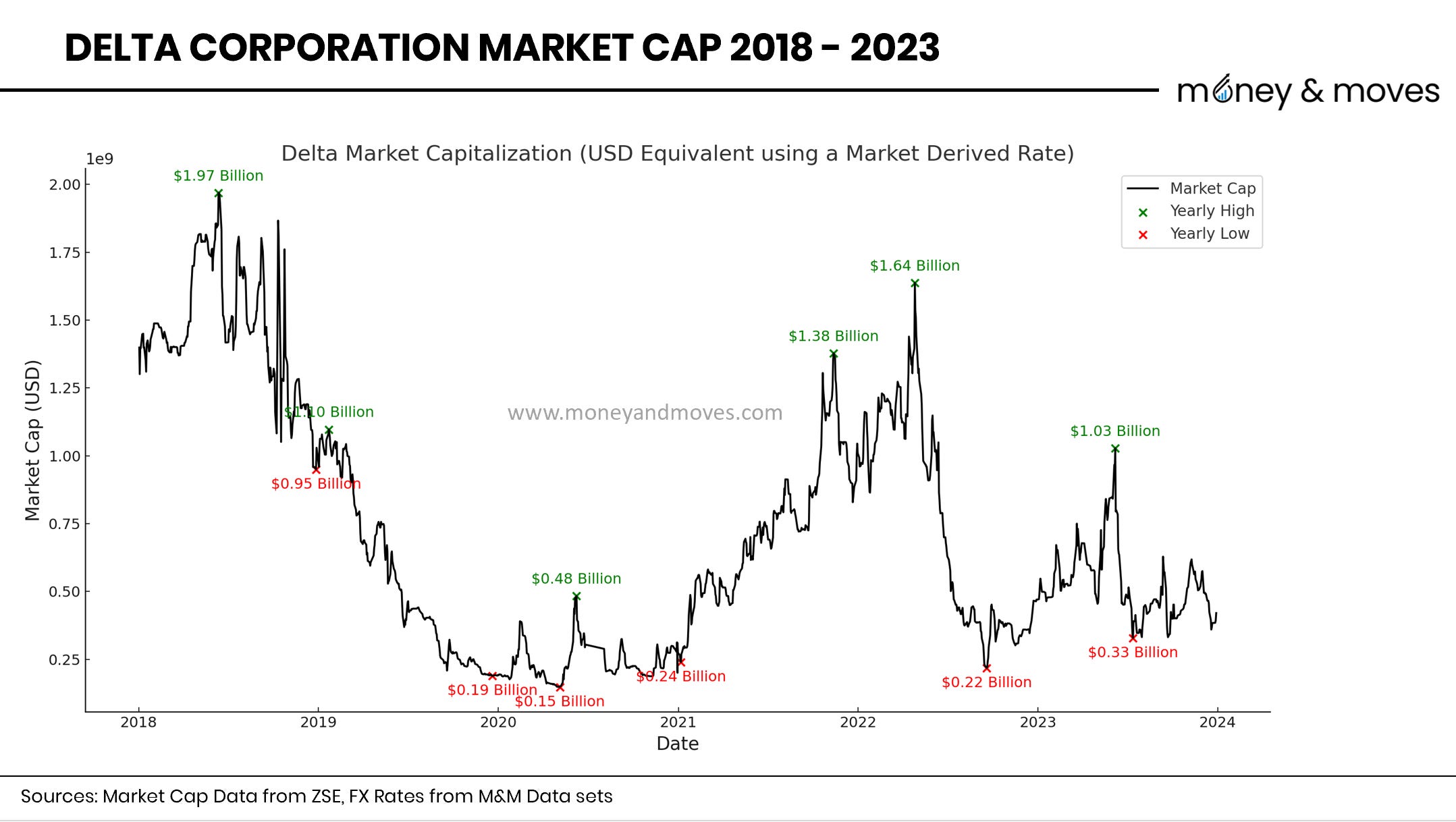

The chart below shows beverage maker Delta Corporation's market capitalisation (market cap) between 2018 and 2023. The green text shows the highest market cap each year, and the red text shows the lowest market cap in that year. All amounts are converted to USD equivalent using the market-derived rate on the day.

What you see are significant swings in value, often within the same year, that are not related to any changes in the company's intrinsic value. Throughout this period, Delta Corporation steadily increased its volumes and generated profits.

It also seems that anytime Delta’s market cap went below $300 million, it corrected upwards, sometimes reaching 5x the previous market cap within 12-18 months. This is not possible in the property market.

Property prices tend to increase slowly and don’t allow you to buy and sell quickly. For exceptional gains, stocks have much more upside.

Where’s the Money? What’s the Move?

Property still seems the most resilient investment option for a “safer” investment. As mentioned in the last article, there will probably be at least another 2-3 years before a slowdown.

However, just because an asset class has performed well does not mean all property investments are good.

The other issue is that the property requires a significant upfront investment and tied-down capital. One can become asset-rich but cash-poor, as it can take time to sell a property, and if it's vacant, it still requires cash to pay expenses.

For Brave Value Investors, Stocks Present an Opportunity

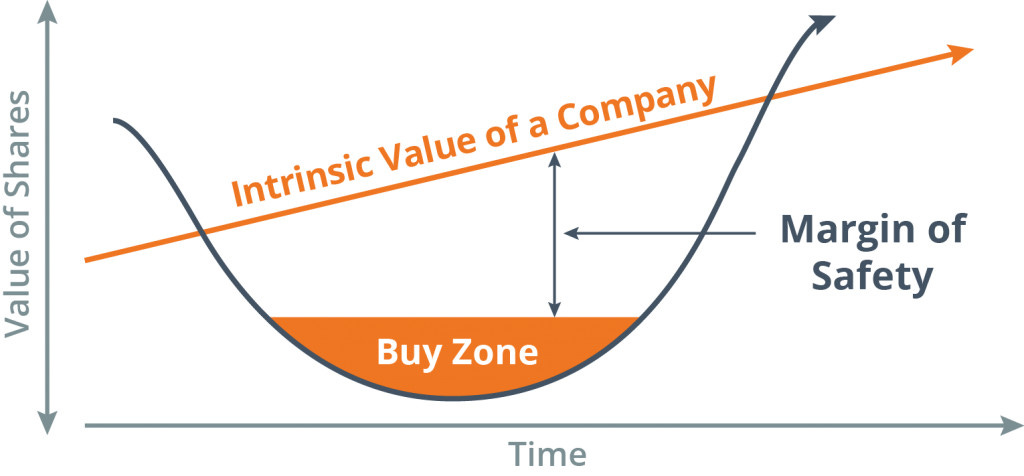

Value investing has been popularised in finance by people such as Warren Buffett, an early mentee of Benjamin Graham, who is considered the father of value investing.

In its simple form, the idea is to buy stocks significantly below their intrinsic value. In my last article, I highlighted one potential example.

The key is to find companies where the gap between value and price is so big that even if you are wrong, there is a large margin of safety.

These opportunities exist in the Zimbabwean context, and I think they are more likely to involve stocks than property.

The tricky part with all these investments is the risk.

However, risk is relative and also personal. So, depending on where you stand, the trade-off could be worthwhile? What do you think?

Thanks for reading; if you found this helpful, please forward this article to someone in your network and subscribe to the newsletter if you have not already done so. It’s completely free.

PS: I am working with publicly available information, so I may be missing something from my analysis or might be incorrect.

Greetings Tinashe

Was in the middle of posting a comment but seem to have lost what I was working on when went back to check on something you had said.

Not to worry will try to recap -

* no need to apologize for for being incorrect - you are asking questions, provoking thoughts and opinions. Think like an economist who spendsr time today explaining how they will be able to tell you tomorrow why what they told you yesterday did not work out.

* in our view critical issues in the analysis must be : period of the investment. liquidity and interim returns.

At the risk of over-simplification (we are new-comers to your stack so have no idea of the degree of sophistication of your readers) property is usually for the long-term (as the form of financing its acquisition usually mirrors); while stocks can also have a long-term view (which is at the heart of the Warren Buffett approach you mentioned), they are frequently held for much shorter periods (especially by share-traders, which also has a taxation consequence). We'll return to Buffett later.

Liquidity rests on the side of stocks. Property purchases also tend to be for larger amounts (you can invest a few dollars at a time in stocks, but you can't buy properties cheaply!). And when it comes to listed stocks there are frequently purchasers waiting in line (depends on your price point and what other stocks within a price-range around that are also available).

Property sales tend to be more difficult to achieve.

Tastes and style change over time and generational attitudes towards property ownership may also change. So for example in South Africa there are many farms on sale at any given time and one of the reasons is that the "younger generation" have gone off to seek fame and fortune in what they have perceived as being "greener pastures".

As we frequently put it : No-one woke up this morning and said: "I just can't wait to go farming at .........(insert your place name!".

And of course in both instances you never make a profit or a loss until you actually sell!

With regard to interim returns the position is a lot more tricky.

Is your property "income-producing" during the period of your investment?

What dividends are you likely to receive from the company?

One of the legs of Warren Buffet's investing style is to place a premium on stocks that have been (or have the potential to) declare dividends on a regular basis.

Also with some types of property maturity can be a blessing or a curse - fruit farmers for example may experience a period of waiting for their trees to reach optimum production and then after certain number of years they need replacing (of course products produced by a company can also go out of style, be rendered obsolete by technological advances etc) so timing of the sale of the property could also affect the return (what potential does the purchaser have to achieve an interim return before realising the asset whether stocks or property could be a critical factor).

And then we have the issue of external factors over which the investor has no (or little control) - changes in government (local and abroad!), economic cycles, natural events.

Currently everyone is trying to deal with the impact of the "tariff" wars.

We are currently working on a book that will be published at the end of May - "Tariff and Stock Prices" which will be available in electronic format for only US$ 4,99. But if your readers place an order and pay now we'll give to them for only US$ 3,99 (ie a 20% discount). Just email us at legaleagles @srvalley.co.za with the words "Tinashe of Money & Moves sent me here" and we'll get back to you to discuss the logistics. Payment will be via Paypal.

Finally talking again of Warren Buffet - we notice he has announced he is leaving office at the end of the year.

Kind Regards

Graeme and Veldra Fraser

www.companylawtoday.co.za

That's true reflection of what actually happened