Delta Corporation vs Varun Beverages

The Battle for Zimbabwe’s Beverage Market

In Part 1, we talked about how Delta performed well in its financial results for the year ended 31 March 2026, showing growth across all key metrics: revenue, volumes sold, profit and cash flow generation.

I did, however, mention two risks to watch. One is taxation. The other is the weakness in their Non-Alcoholic Beverages segment.

In this segment, Delta competes closely with the Zimbabwean arm of Varun Beverages, the largest PepsiCo bottler in the world outside the United States.

Comparing these two businesses helps you understand the risk and opportunity that lies ahead for Delta.

In Part 2, we look at that competition in detail, and we also touch on the tax dispute sitting above the business.

Let’s Unpack!

Varun Beverages: From Zero to a Hundred

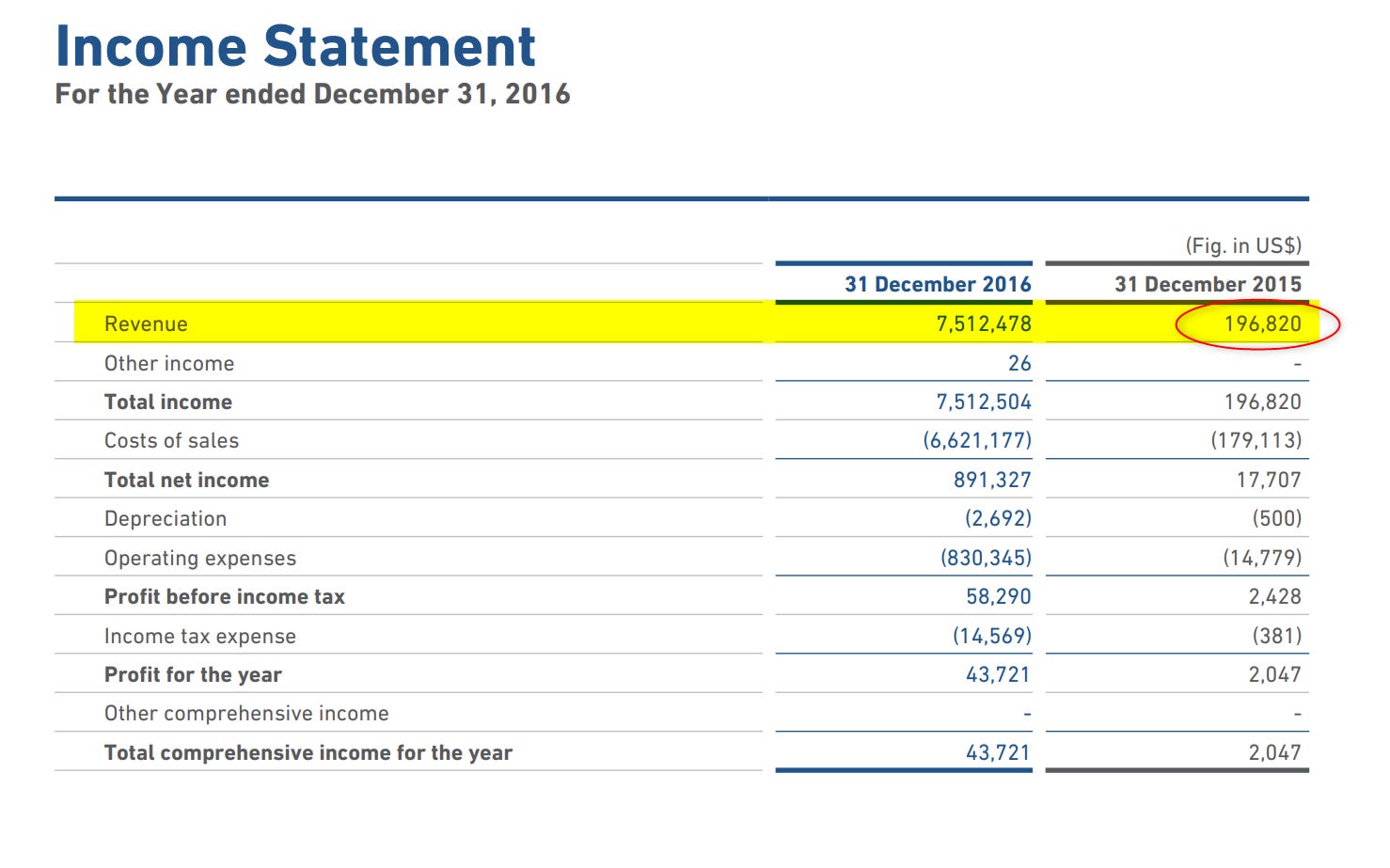

Varun Beverages entered the Zimbabwean market in 2015.

They came in with a plan to invest over $110 million and build a plant capable of producing 80 million bottles and cans per month.

To attract that kind of investment, the government gave Varun Special Economic Zone (SEZ) status. The benefits were significant.

Zero corporate tax for the first five years of operation

15% corporate tax rate thereafter, compared to the standard rate of 25%

Duty-free importation of capital equipment

Duty-free importation of raw materials not produced locally

The benefits are worth millions, with the corporate tax benefit alone saving more than $15m over the last three years, and Varun has put these benefits to good use.

When Varun started operations, their revenue was just under $200,000. Ten years later, that same business generates close to $200 million in annual revenue.

This tells you something about emerging markets. If you have a business meeting a broad need, at a competitive price point, you can scale extremely quickly.

The SEZ status gave Varun a strong platform to build from, and they used it aggressively.

The Head-to-Head: Three Years of Data

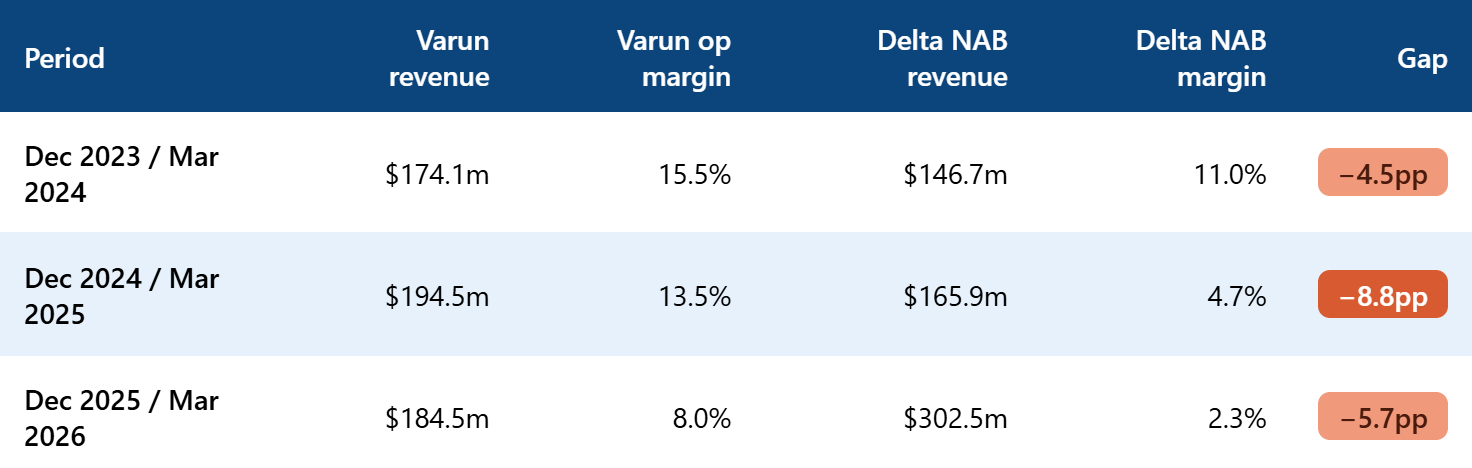

The table below compares Delta’s Non-Alcoholic Beverages segment against Varun Beverages Zimbabwe across the last three comparable financial years.

A few things are worth noting here.

Before the Sugar Tax, the gap was already there.

Let's start by looking at the years ended March 2024 and Dec 2023 (note the companies don’t have the same year-end, but this comparison overlaps by nine months, and so this is the best reference point)

This is the cleanest comparison because neither period carries the full weight of the sugar tax, which only came in from January 2024.

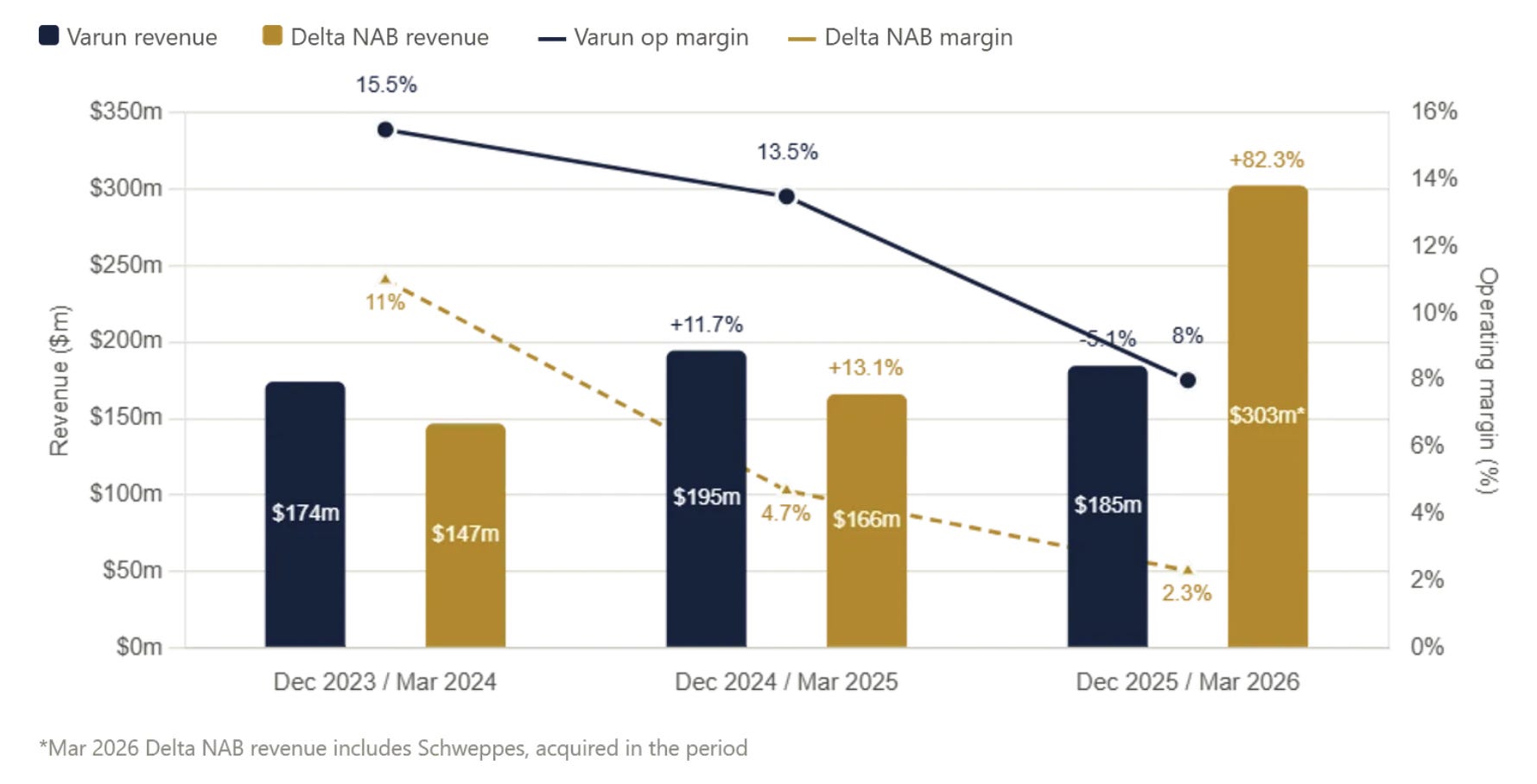

Even in that pre-sugar tax environment, Varun’s operating margin was 15.5% compared to Delta’s 11.0%. A gap of 4.5 percentage points. This indicates that, as a business, Varun was generally more profitable than Delta’s Non-Alcoholic Business.

This makes sense for a few reasons.

First, the SEZ benefits we mentioned covered imported input costs as well and so would have direct cost benefit.

Second, plant efficiency. Delta has been bottling Coca-Cola products since the 1950s. Varun built their plant less than ten years ago.

Newer plants tend to be more energy efficient, produce less waste, and require less maintenance. I would be surprised if Delta’s bottling plant is more efficient than Varun’s.

Third, concentrate costs. Coca-Cola is the strongest beverage brand in the world. I would imagine they place a premium on that brand when pricing the concentrate, the key ingredient needed to make Coca-Cola.

These three advantages together explain why Varun could come in with an aggressive pricing model and still make good money in the early days. They had a lower cost base from day one.

When the Sugar Tax Hit: Delta Took a Bigger Fall

What happened in the year ended March 2025 for Delta and December 2024 for Varun is where it gets really interesting.

Delta’s margins fell from 11.0% to 4.7%. Varun’s fell from 15.5% to 13.5%.

Both companies faced the same tax. But Delta’s fall was far more severe.

Part of the answer is likely product mix. Varun had been aggressively building their bottled water brand, Aquaclear, which carries no sugar tax. This is an area that Delta was not as strong in.

There is also a bit of timing.

The Sugar Tax payable before 9 February 2024 was waived, so for Varun’s December 2024 year-end, they would have had just over a month of trading without it, whereas for Delta’s comparative period, year ended March 2025, the tax would have been fully in effect.

However, the above was to be expected, but what happened in 2025 is surprising.

The Most Recent Numbers: The Tables Are Turning

When we look at the most recent period. Dec 2025 for Varun and March 2026 for Delta.

Varun’s revenue fell from $194.5 million to $184.5 million. A 5.2% decline. Their operating profit nearly halved, from $26.3 million to $14.8 million. Their operating margin dropped from 13.5% to 8.0%.

Delta’s sparkling beverages business grew by about 15% (the 82% includes Schweppes, so it is not comparable).

This is surprising; I always expected a slowdown in growth from Varun, as you can’t keep growing at the rate they were.

But to decrease revenue by 5% while your competitor increases by about 15% is a concern.

There are a few things that I guess could have happened, and most likely all together.

The first is pricing. As you can tell from Delta’s slim margins of 2.3%, the Non-Alcoholic Beverages Segment has been pricing aggressively to protect and grow market share.

The second is brand.

When Coke and Pepsi are at a similar price point, most Zimbabweans will choose Coke. The same goes for Sprite over 7Up and Fanta over Mirinda. Delta’s portfolio carries the stronger consumer preference, and at competitive pricing, that preference converts into volume.

This is where the advantage of a diversified portfolio comes in.

Delta’s lager beer business generates a 35.6% operating margin and generates lots of cash, so they can afford to digest lower margins in the soft drinks pricing for a season.

Varun does not have that optionality yet. This may explain why they have been talking to Carlsberg to enter into the beer business

So with Varun’s numbers dropping and Delta seemingly gaining market share, what does that mean?

The Opportunity in Numbers

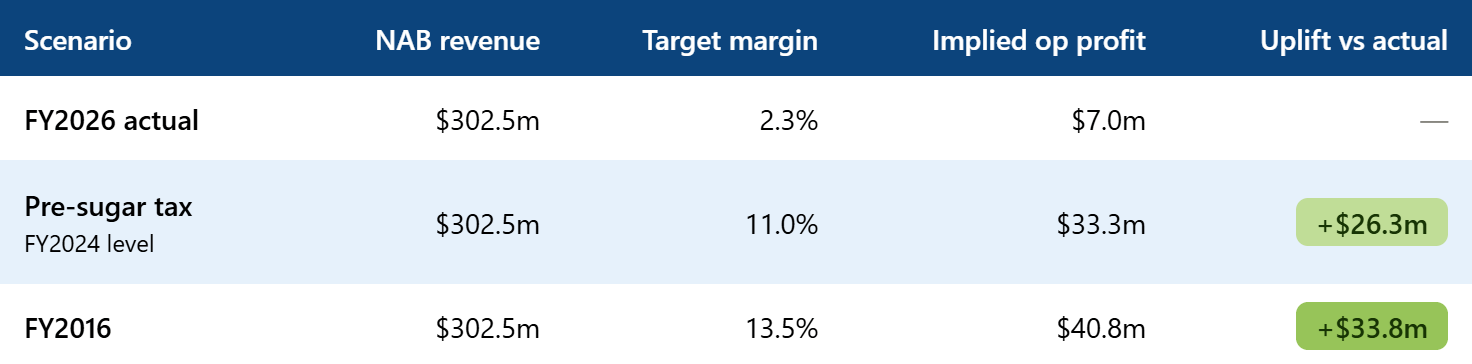

If Delta’s Non-Alcoholic Beverages segment can get back close to the margins it was delivering before the sugar tax, the numbers look very different.

Getting back to even the FY2024 pre-sugar tax margin would add approximately $26 million to operating profit. At Delta’s effective tax rate of 27.6%, that flows through to roughly $19 million in additional net income.

That is the opportunity. Can Delta execute?

With the sugar tax still in place, it will be hard to get back to the same level, but if growth is maintained and they can reach even an 8% - 9% margin, that is still about $20 million in additional net income.

There is one more issue sitting above all of this that readers need to keep in mind.

The Tax Dispute: ZIMRA vs Delta

The dispute with Zimra is essentially about what currency taxes should have been paid in.

ZIMRA assessed Delta for an additional US$97 million in foreign currency taxes for the 2019–2024 period. Delta contends that its historical tax payments in local currency were legally compliant based on the conversion frameworks active at the time; ZIMRA’s position is that prior local currency payments cannot be used to offset or settle liabilities that were strictly due in USD.

Predicting the outcome here is genuinely difficult.

Tax authorities globally tend to concentrate enforcement resources on their largest taxpayers, simply because the collection efficiency is higher; a handful of large assessments can move the needle on revenue targets in a way that thousands of small ones can’t.

Delta, as one of Zimbabwe’s largest taxpayers, sits squarely in that category, and a case of this size and complexity is the kind ZIMRA would prioritise.

At the same time, a $100m assessment on one of the country’s largest and most visible corporates carries its own considerations, balancing revenue collection against the broader signal it sends to large taxpayers and investors.

Often, such cases are settled out of court through a negotiated arrangement, as in South Africa, where Anglo’s Kumba Iron Ore and the South African Revenue Service reached a R2.5 billion settlement.

If the assessment is upheld in full, the impact on Delta would be significant. Last year, Delta budgeted about $70 million in capital expenditure; the $97 million exceeds a full capex cycle.

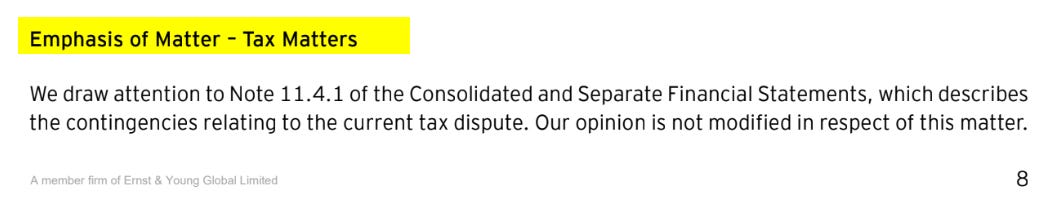

This is one to watch, which is why the auditors flagged it as an emphasis of matter.

This is basically when the auditors say the numbers look fine, but pay attention to this one thing that could have a big impact on how you see things.

Where’s the Money? What’s the Move?

The best businesses have a solid base and attractive upside.

Delta’s solid base is the alcoholic beverages business, particularly lager beer, at a 35.6% operating margin. That business is exceptional and largely unchallenged for now. One could make an investment case on that business alone.

The upside is in Non-Alcoholic Beverages, which currently has margins of 2%.

If you believe Delta can win the soft drinks battle, integrate Schweppes smoothly and claw back margin, the earnings recovery story starts to look compelling.

If you believe the challenges in Non-Alcoholic Beverages are structural and will persist, then you are essentially relying on the alcoholic business alone to carry the valuation.

All in all, with consistent double-digit growth, a dominant market position and a forward P/E ratio of about 7-8, there does still seem to be some room for Delta to continue to grow.

What do you think?

Thanks for reading. If you found this useful, please forward it to someone in your network.

P.S. I am working with publicly available information. I could be wrong or missing something.