Econet's Delisting: 100 Days Later

100 days after Zimbabwe's biggest corporate action, here's what the exit offer, InfraCo's listing, and Econet's own results actually show.

It’s been 100 days since Econet was delisted, the biggest corporate action in Zimbabwean capital markets history.

Here are three things the first 100 days have told us.

Let’s unpack!

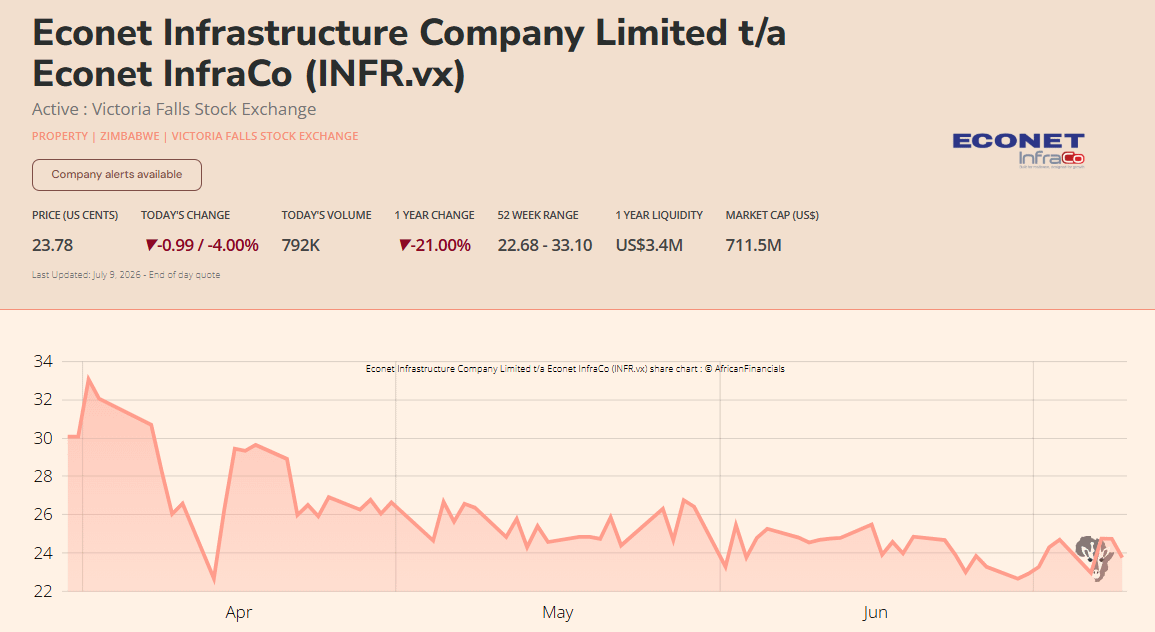

Econet InfraCo Fell, But It Could Have Been Worse

As detailed when we first discussed the delisting, part of the transaction involved the spinning out and listing of Econet InfraCo on the VFEX at a $1 billion valuation.

The general consensus was that the valuation was on the high side, and so, as expected, the stock dropped.

From an exit offer price of 33c, it opened at 30c, and today, the stock is at about 24c, roughly a 25% drop from that 33c reference point.

This is a big drop, especially when you consider that of the other 15 stocks on the VFEX, 10 have year-to-date gains of over 15%, with Innscor and its cousins (Padenga, Simbisa etc) with returns over 40%.

At the same time, a 25% drop is not that bad. It definitely could have been worse.

Depending on your view of the valuation, the stock could have dropped by 50%.

Perhaps part of the reason the stock didn’t drop further is that there was some sort of support provided. This can happen when a company or related parties buy back the shares at a certain level.

If this were the case, it is not a bad thing.

In fact, I think it could have been seen as ideal, as it would mean shareholders who opted for the exit offer were able to exit close to the 33c value their offer was priced on, which was the main concern when the valuation first looked high.

This takes us back to the analysis we did when the offer was on the table, where we said the best approach seemed to be a hybrid one: take part of the exit offer for liquidity, and remain in the delisted entity for the rest. Here is the quote

The approach that produces the best risk-adjusted outcome across all three considerations is probably a hybrid — take the exit offer on a portion of your shares to lock in liquidity, while retaining the rest in the delisted Econet to participate in the year-one buyback and the long-term growth story.

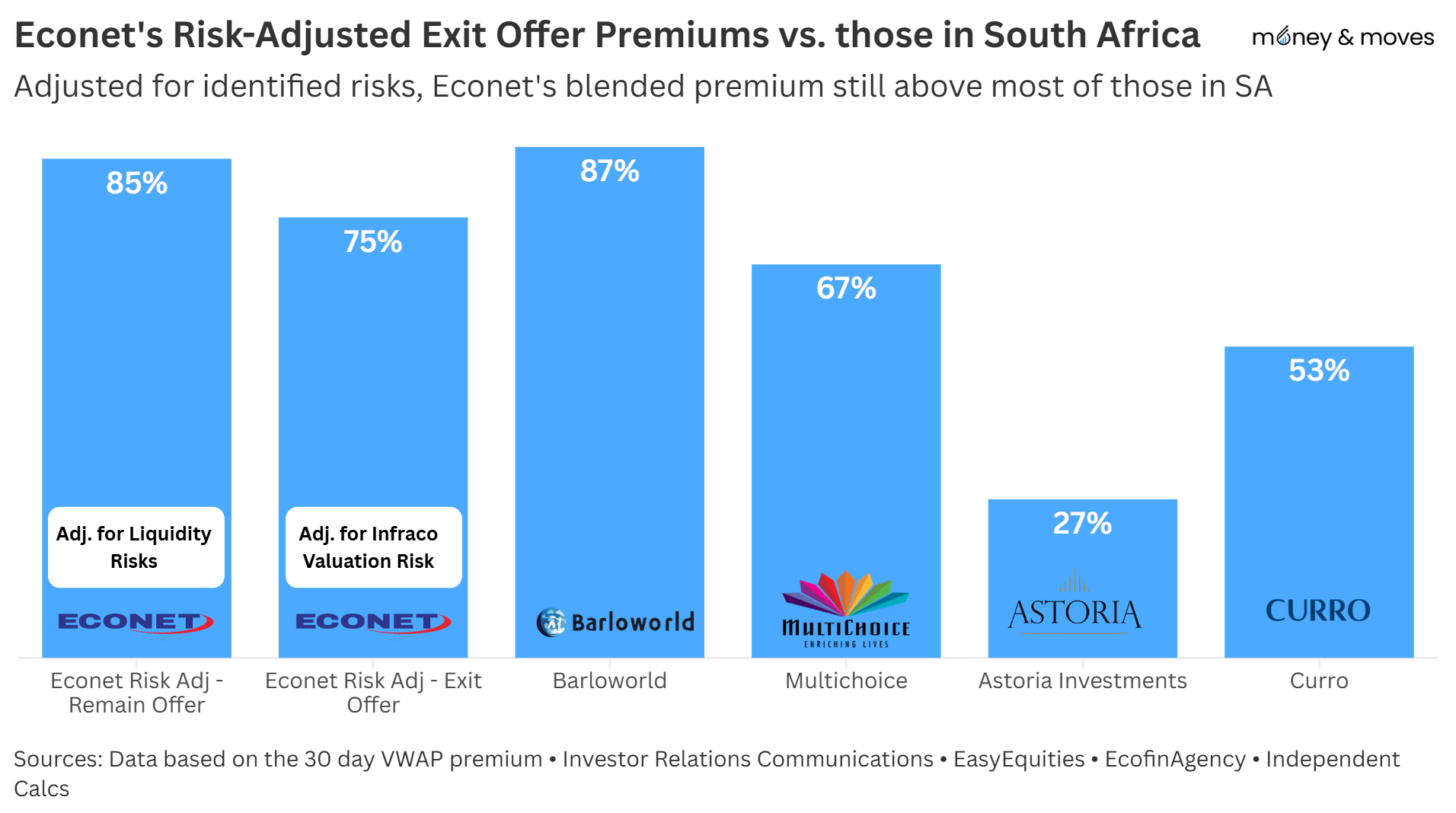

When arriving at that conclusion, we modelled the exit offer at a conservative 18c per share. So even if you sold your InfraCo share for 20c to 25c, you still came out with decent returns, generally higher than most exit offers among South African peers.

It’s also worth noting that since the delisting, there have been much lower exit offers elsewhere.

First Mutual Properties, for example, delisted with an exit offer premium of only 5.1% of the 30-day VWAP. Econet’s offer premium, even after adjusting for the risks, was 85%.

So overall it seems the exit offer wasn’t a bad deal, but what about those who remained in the delisted Econet?

Econet’s First Results As a Delisted Company

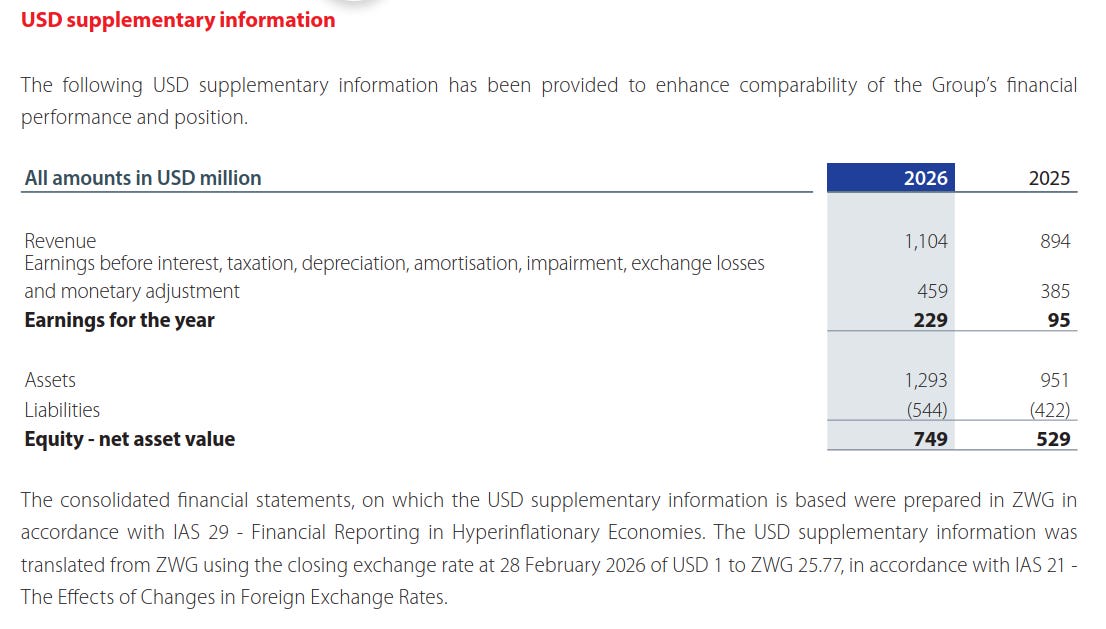

So if you remained in the delisted entity, you would have seen Econet’s annual results.

In short, the results were pretty good; revenue was up 24%, and earnings (profit) more than doubled.

We had a hint of this potential at half-year, but it’s now official that Econet has joined the $1 billion revenue club, solidifying Zim’s current big three: Delta, Insccor and Econet.

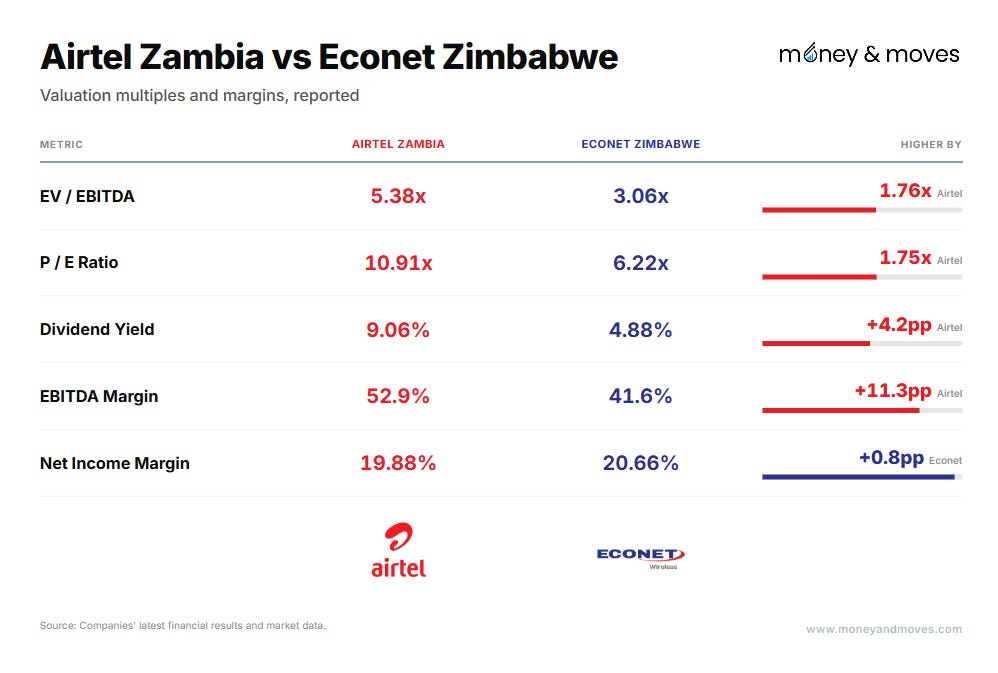

For benchmarking against peers, I like to use Airtel Zambia. Econet has no local peer, and Zimbabwe is often assigned the same country risk premium as Zambia as a proxy (an approach valuation expert Aswath Damodaran has used).

Below are some of the key financial metrics for the two companies. For Econet’s valuation, we’ve used 50c per share, the floor price Econet has committed to for its buyback, as a proxy for its market value.

What you see above is that Econet’s EV/EBITDA (a valuation measure) at 3x is still quite a bit lower than Airtel Zambia’s, with Airtel trading at about a 76% premium on that measure.

The same goes for the P/E ratio. Apply that same premium to Econet and the “share price” would be worth about 88c, which would put Econet’s market cap at just over $2.6 billion.

However, this would assume that the “premium” Airtel is equally applicable to Econet, which may not be the case.

A company with better long-term prospects can rightly trade at a premium that another company can not claim.

There is some case to be made for Airtel Zambia’s premium over Econet. Econet is a great business, but one advantage Airtel has is that it’s a more profitable business despite charging consumers less.

For example, for 5GB of data, Econet charges $9. With Airtel, you can get 7.5GB for $5.50. So more for less.

There could be good reasons for the pricing difference, but it does show Airtel is able to generate better EBITDA margins with lower pricing. That’s always a better position to be in, especially in emerging markets.

The other thing is, Econet has to deal with the Zimbabwe overhang. Despite a much better economic performance over the last few years, there is still that hyperinflation-induced trauma that things will suddenly go wrong. This weighs on a lot of valuations.

But with all that said, even now Econet could still be undervalued.

This makes it interesting; so we have two Econets in the same market, and one is possibly overvalued, and the other is possibly undervalued!

Valuations in Zimbabwe and Market Inefficiency.

The efficient market hypothesis assumes that markets get pricing right because all available information is already reflected in the price. It’s an influential enough idea that Eugene Fama won the Nobel Prize in Economics largely for it.

Econet is a case where that assumption doesn’t hold. Econet was for a long time valued too low, while Econet Infraco has probably been valued too high.

Illiquid markets, where the number of regular buyers and sellers is low, are especially prone to this. Whether you want to exit or enter a position, you often can’t, so mispricing can sit there for a long time instead of correcting quickly. This is not fun.

But that same inefficiency is where the opportunity lives. Econet’s share price was trading at around 10c at some point last year, and now it’s worth 50c at a minimum. That’s a good return for anyone who spotted it early.

Where’s the Money? What’s the Move?

Last year there was a sea of undervalued, mispriced stocks, many of which we covered here. It’s harder to find those opportunities now. Relative to last year, there are probably more stocks that are fairly valued or overvalued than undervalued.

It’s also worth widening the search to other African markets. Airtel Zambia, for example, which we discussed, has been up over 300% since the start of last year and still offers a 9% dividend yield.

Mispricing happens a lot in African markets. The question is whether you can benefit from it. Those who bought Econet last year certainly did.

P.S. I am working with publicly available information, so I could be wrong or missing something. This is for informational purposes only, not financial advice, so do your own research before acting on anything here. Thanks for reading!