Econet's Delisting: Where's the Money? What's the Move?

Not all returns are created equal. Here's the risk-adjusted framework every shareholder needs to consider before voting.

Recently we unpacked everything you need to know about Econet’s delisting. This week is the big day when shareholders must vote on which way to go.

Today, we tackle the more practical question: what moves can you make to navigate the delisting to make money?

But before we dive in, there’s an important idea worth establishing upfront, because it changes how you should think about everything that follows.

The Most Important Thing in Investing

Consider two investors.

Investor A takes US$1,000 and, in three years, turns it into US$3,000.

Investor B also takes US$1,000 and, over the same period, turns it into US$1,500.

On paper, Investor A wins easily. But what if I told you that Investor A got their return by buying lottery tickets, while Investor B bought high-quality blue-chip stocks?

Suddenly, the picture changes. Investor B is the better investor, not because they made more money, but because they took on much less risk to get their returns.

This is one of the central ideas in investing: what matters most is not just returns but risk-adjusted returns. If you miss this idea, you may make money in the short term through luck, but it usually doesn’t end well in the long run.

This brings us directly to the Econet delisting.

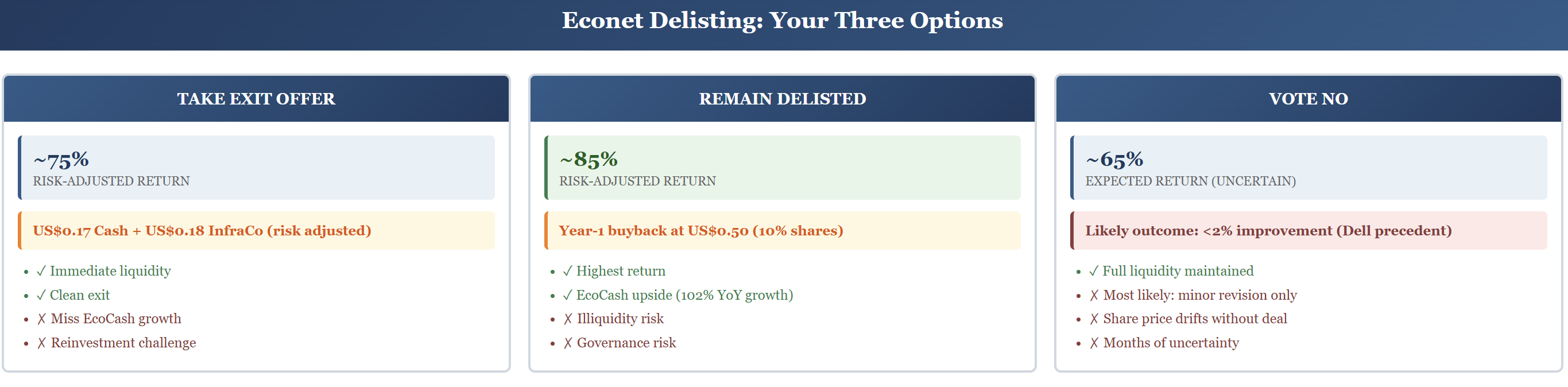

There are three paths available to you as a shareholder: take the exit offer, remain in the delisted Econet, or vote against the delisting entirely.

What presents the best risk-adjusted returns?

To work this out, we will do two things. First, we will calculate the baseline return for each option using numbers we can quantify. Then we will layer on the hidden risks and opportunities that the numbers alone don’t capture.

For all calculations, we will use the 30-day VWAP of US$0.20 as our reference cost price. The VWAP (Volume Weighted Average Price) is basically the real value Econet shares actually traded at before the talk of corporate actions and delisting started.

While everyone will have different cost bases, this is a comparable benchmark that helps to make an assessment.

Warning, this may get quite technical, but when you have potentially the most impactful corporate action in the country’s history, it’s worthwhile working through it.

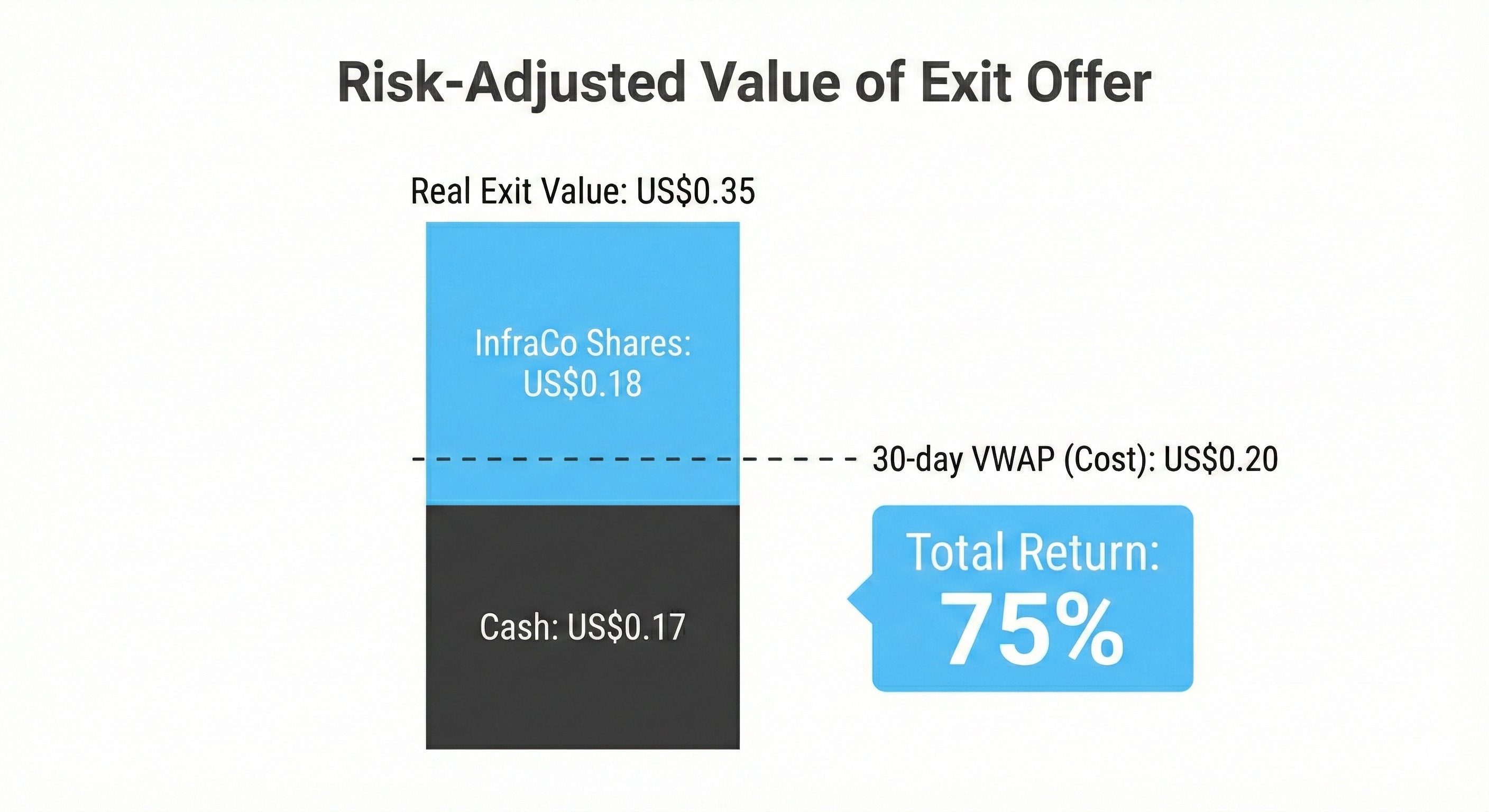

Path 1: Take the Exit Offer

This is the simplest path to calculate, so let’s start here.

The headline offer is US$0.17 in cash plus US$0.33 in Econet InfraCo shares, a combined stated value of US$0.50.

Earlier, we laid out the data suggesting InfraCo is overvalued at the stated US$1 billion.

Last week, FBC Securities put out a note with their own range of scenarios — their most optimistic case came in at US$0.36 per InfraCo share and their worst case at US$0.18.

We will work with US$0.18 per share, as, from a risk management perspective, it makes sense to plan around the downside, and based on earlier analysis, this number looks more aligned to expectations.

Under this scenario, the real value of the exit offer looks like this:

Cash US$0.17 + InfraCo shares US$0.18 = real exit value US$0.35

What’s the return?

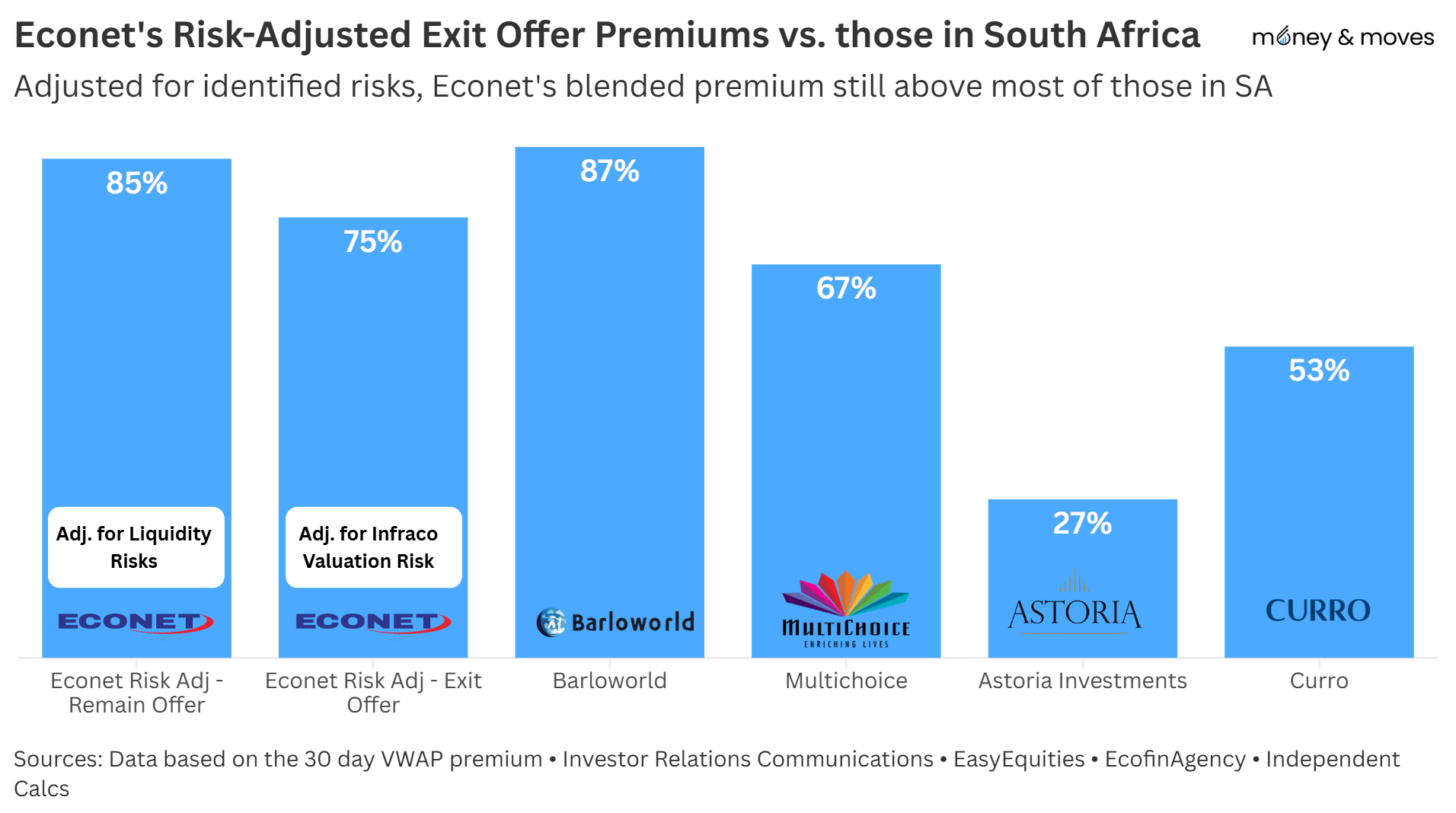

Starting from our 30-day VWAP of US$0.20, a real exit value of US$0.35 represents a 75% return.

What about tax?

This is where the exit offer has an advantage. Because of special rules for the VFEX and ZSE, the amount of tax to be incurred is negligible.

This means the after-tax exit offer return is still about 75%.

Path 2: Remain in the Delisted Econet

This path is more complex to evaluate.

The key mechanism here is the year-one share buyback. Econet has planned to repurchase up to 10% of outstanding shares after 12 months at a floor price of US$0.50.

So the question becomes: what is that US$0.50 actually worth in today’s money, after tax and after properly accounting for the risks involved?

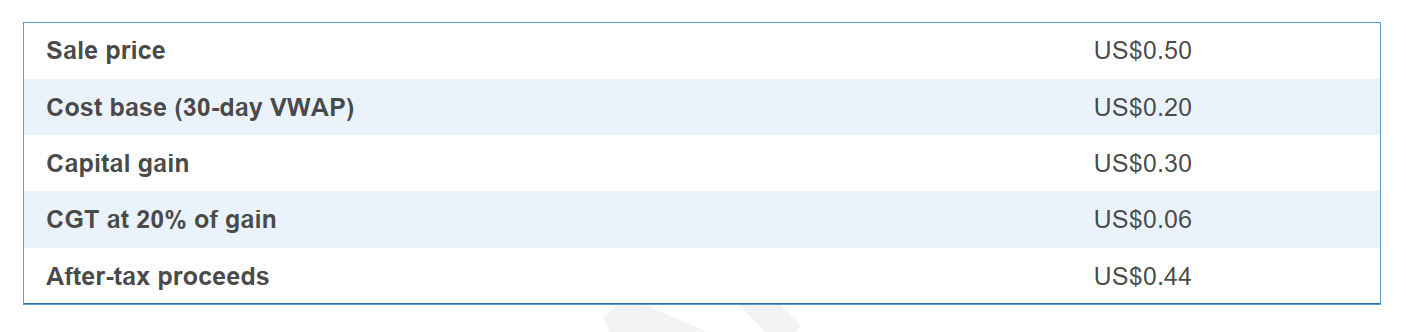

Step 1: Tax

Once Econet delists, its shares become unlisted securities.

Under Zimbabwe’s Capital Gains Tax rules, unlisted shares attract a CGT rate of 20% applied to the capital gain.

Using our 30-day VWAP of US$0.20 as our assumed cost base:

Step 2: Discount rate

A dollar today is worth more than a dollar in a year’s time and so . We need a discount rate that reflects two things. First, the opportunity cost of waiting: if you put your money in a savings account today, you could earn about 12% per year in USD. We’re using the Omari savings account as a reference.

Second, the risk of holding an illiquid, unlisted security in Zimbabwe. To capture this, we can apply Zimbabwe’s country risk premium of 11.66%. PS, this is more subjective, but it was the best way to quantify the risks into a defendable number.

Combined discount rate: 23.66%

Discounting the after-tax proceeds:

US$0.44 ÷ 1.2366 = US$0.356

Step 3: Dividends

Econet paid a total of 1.76 US cents per share in dividends in FY2025 (year ended February 2025).

However, the business has experienced significant growth. Revenue for the most recent half-year increased by nearly 40%, with profits rising by over 300%.

That growth would normally mean a much bigger dividend.

However, Econet also needs to save cash to fund the exit offer and the year-one buyback, commitments that could require up to US$200 million in total.

Balancing these two factors, a dividend of approximately 2.00 US cents per share is a reasonable estimate for the coming year, an increase from 1.76c that reflects the earnings growth while acknowledging the cash preservation pressure.

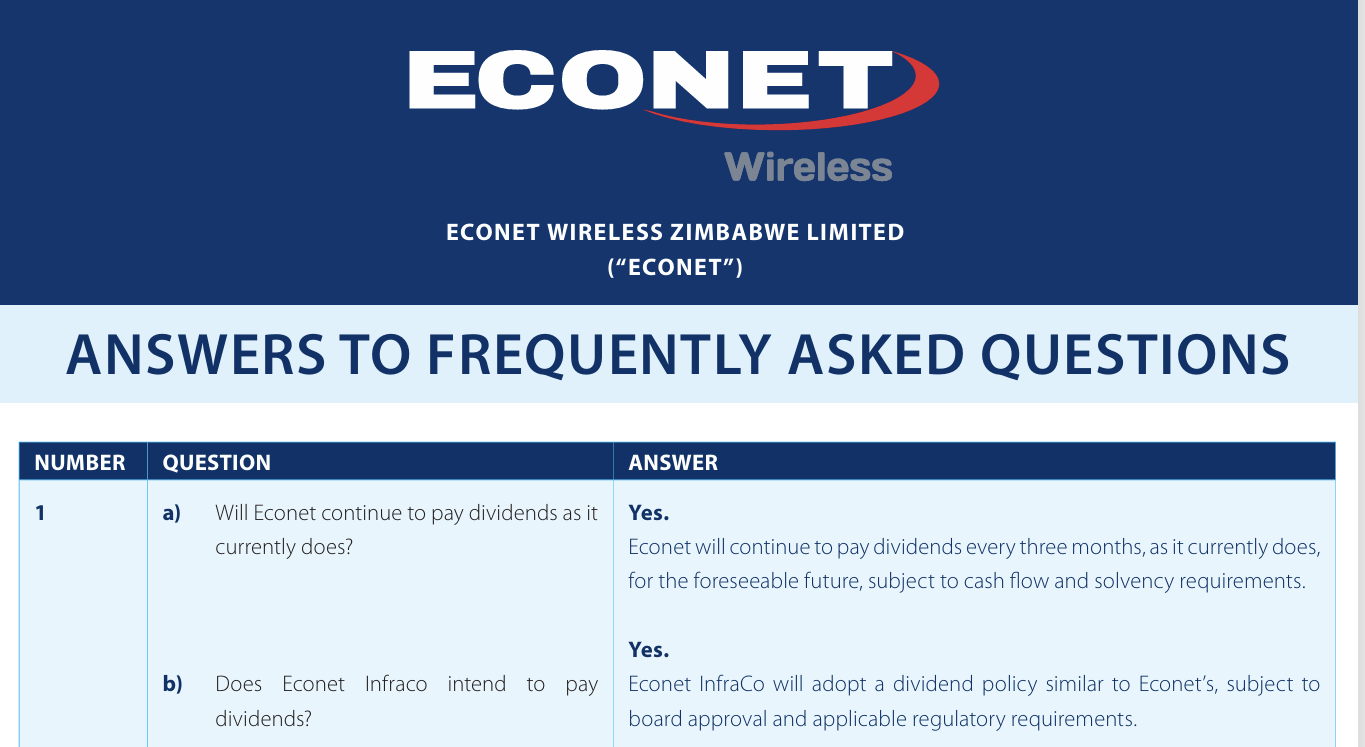

It is also worth noting that Econet recently published an FAQ confirming they intend to continue paying dividends after delisting, which provides some additional comfort on this point.

Adding the present value of dividends (~US$0.018) to the discounted after-tax proceeds:

Total risk-adjusted present value of the remaining option: approximately US$0.374, call it US$0.37.

Return from the 30-day VWAP of US$0.20: approximately 85%.

On paper, this is better than the exit offer. But the gap is narrower than it first appears.

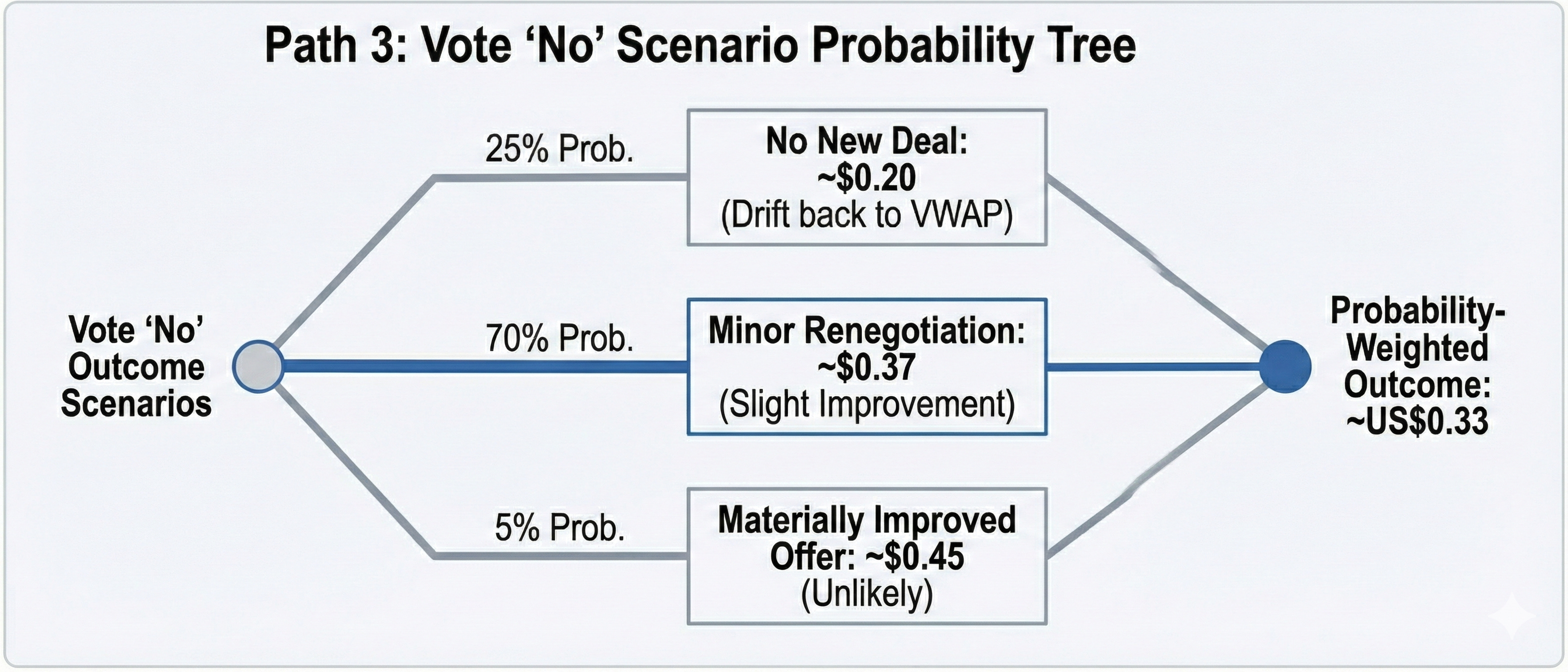

Path 3: Vote Against the Delisting

This is the hardest to quantify — and the highest variance of the three options.

The opportunity is that a “no” vote could force Econet back to the table with a better offer. The risk is equally straightforward: it might not. And unlike the other two paths, there is no defined timeline. There could be months of waiting before anything moves.

Rather than using a single reference price, we will model three scenarios explicitly and weight them by probability.

Scenario 1 — No new deal (25%): The board holds firm, no improved offer materialises, and the share price drifts back toward the US$0.20 VWAP — what the market priced Econet at before any of this began.

Scenario 2 — Minor renegotiation (70%): The most probable outcome (I explain more why in the next section using Dell Computers as a Case Study). The board makes slight adjustments, enough to get the vote over the line on a second attempt, but not enough to materially change the economics. Any revised offer would need to clear the exit offer’s risk-adjusted value of US$0.35 to be worth accepting, so we estimate this outcome at approximately US$0.37. This, however, would take a lot of time, which may see the real value of the US$0.37 being less.

Scenario 3 — Materially improved offer (5%): The board proposes a significantly better deal, say worth US$0.45. I would imagine this is the least likely scenario, as the board strongly believes that this is a fair offer and they probably could made strong arguments in this direction.

Probability-weighted outcome:

(25% × US$0.20) + (70% × US$0.37) + (5% × US$0.45) = ~US$0.33 which is about a 65% return.

Putting it all together

So, putting it all together, this is what the picture would look like based on our quantitative risk-adjusted returns.

However, even with that, there are more qualitative risks we need to consider.

The Hidden Risks and Opportunities That Are Hard To Quantify

The numbers above give you a framework. But there are some things the spreadsheet doesn’t capture.

Exit Offer: The Reinvestment Problem

When you accept the exit offer, you receive InfraCo shares that you can sell relatively quickly after the VFEX listing. From a liquidity perspective, the exit offer is far better than the other options.

But there is a practical question worth asking directly: if you take the cash, where does it go?

Last year, the VFEX had several obviously undervalued companies. Innscor, for example, when we first covered Innscor, it was trading below US$0.50 per share at the time.

Today it trades at approximately US$1.03 per share. This is the case with many stocks on the VFEX.

If you take the exit offer, you will be redeploying cash into a market that does not have many great options right now.

That is not a reason to stay in Econet by default, but it is worth factoring into the decision.

Remain Option: The Upside and The Real Risks

The upside: By remaining in the delisted Econet, you are staying invested in a fast-growing business with meaningful further upside. The fastest-growing part of the group is EcoCash. Mobile money revenues grew 102% last year, and the long-term potential of the business is substantial.

To put that in context: when the EcoCash business was separately listed on the ZSE as Cassava SmarTech, the market at its peak valued it at over US$1 billion on its own. That business is now back inside Econet, and at the current implied valuation, it is arguably not being fully credited for its growth trajectory.

As we have seen from Safaricom’s M-Pesa in Kenya, mobile money businesses in Africa can sustain strong growth for extended periods as financial inclusion deepens. This is a good business to be in.

The risk

The liquidity risk is not fully solved by the buy-back and the OTC market. In a listed company, you can sell your shares at any time, at a transparent market price, with settlement within days.

In the delisted Econet, you are dependent on the OTC platform, a board-approved buyer list, and ultimately the year-one buyback, which will only take 10% of all shares, meaning you may not be able to sell all your shares.

After delisting, transfers will no longer be automatic via the ZSE. Sellers will need to comply with CGT requirements directly and, where shares are sold to new investors, obtain board approval before the transfer is registered.

If your circumstances change and you need the money urgently, your options are limited. Even if you are happy to sell at a discount, you may not be able to.

Also, from a governance perspective, there is probably more risk in an unlisted public company than in a listed public company.

Vote No: The Opportunity and The Risks

The best case outcome for a minority shareholder is that the existing US$0.50 offer gets restructured into an all-cash deal.

That is theoretically possible, but genuinely unlikely.

The more probable outcome, if the vote fails, is a minor revision, an extra cent or two in cash, perhaps slightly improved OTC protections that do not materially change the economics.

The Dell Technologies take-private of 2013 illustrates what this dynamic looks like in practice.

Michael Dell owned just 16% of the company and wanted to take it private. He and Silver Lake offered US$13.65 per share. Carl Icahn, one of the most feared shareholder activists in Wall Street history, rejected the offer and launched a full-scale campaign of lawsuits, media pressure, and alternative proposals.

After months of fighting, minorities received US$13.88 in total cash, including a special dividend sweetener Dell added to get the deal over the line.

On the original offer of US$13.65, that is an improvement of less than 2%.

Dell changed the meeting date, adjusted the voting rules, and got his deal done. A 16% founder got his way despite facing one of the most feared activists in history, who, after months of fighting, moved the offer by less than 2%.

Now consider the Econet situation. The controlling shareholders have a larger ownership stake, the market is less mature, shareholder activism is limited, and there is no Carl Icahn (at least none I have heard of) waiting to pounce.

Also, the current offer, while imperfect, still compares well against peers in South Africa. For example, if we used our risk-adjusted returns and compare with similar offers in South Africa, the offer still seems competitive.

What are the realistic chances of forcing a meaningful improvement?

Also, in a failed vote scenario, the share price could fall, and that actually gives the controlling shareholders more leverage, not less. Without the announced deal anchoring the price, the share price could drift back toward pre-cautionary levels.

The controlling shareholders could then return with a revised offer that still represents a premium to the then-current price, but lower in absolute terms than the original US$0.50. Minorities who held out hoping for a better deal could end up accepting less than they would have received by simply taking the original offer.

Where’s the Money? What’s the Move?

The honest answer is that this is a closer call than the headline numbers suggest.

The exit offer delivers about 75% on a risk-adjusted basis with higher certainty, but leaves you redeploying cash into a market without many obvious opportunities right now.

The remain option delivers approximately 85% on a risk-adjusted basis, with exposure to a fast-growing business and real long-term upside from EcoCash. The higher return comes with a catch: illiquidity, governance risk, and the uncertainty that comes with holding an unlisted asset. The upside is higher, but so is the uncertainty.

Voting no is the most complex of the three. Our probability-weighted analysis puts it at approximately US$0.33 below the exit offer in expected value, and with significantly more variance around that number

The approach that produces the best risk-adjusted outcome across all three considerations is probably a hybrid — take the exit offer on a portion of your shares to lock in liquidity, while retaining the rest in the delisted Econet to participate in the year-one buyback and the long-term growth story.

The weighting between the two depends entirely on your liquidity needs. The less you need cash in the near term, the more you can afford to keep in the remain basket.

If you go this route, two things matter.

On the InfraCo shares, watch the market closely in the first week, the opening price will tell you a lot about whether holding or selling immediately is the right call.

On the remain side, be honest with yourself about your cash needs over the next 12 - 18 months, and consider whether there is an appetite among other remaining minorities to engage collectively with the board. Organised minorities are in a meaningfully stronger position than fragmented ones.

Worth noting: if liquidity matters more than returns for you (as it may for some individuals and institutions), then “voting no” could be an option for you, as it's the path that preserves the full liquidity that comes with being listed.

One final observation worth making: by my estimation, the delisted Econet will be one of the largest companies in Africa trading via OTC.

That scale trading on the OTC will inevitably create opportunities from market inefficiencies for the savvy trader. Who knows what manner of financial instruments and transactions can be created on the back of all these shares that may be illiquid?

This has been a complex topic that required a lot of judgment calls. Do your own research, and I would genuinely love to hear your views in the comments, especially if you think I have got something wrong.

There are genuine reasons to take each of the paths; it may end up coming down to preferences and circumstances.

As always, this is not financial advice — it’s analysis based on publicly available information for educational purposes. I may have missed things or got some things wrong, so please call it out in the comments. Do your own research and consult with a qualified adviser before making investment decisions.

Great analysis here👏👏i enjoy reading and learning a lot from your work. Thank you very much