Innscor's Financial Results: It Takes Money to Make Money

In October, I wrote about Innscor’s results in “Money Never Sleeps.” The story was about incredible revenue growth. A billion-dollar company growing at 19%. But there was a problem. Profitability was slipping. Margins had fallen from around 15% a few years back to 9%.

Six months later, the margins appear to be coming back. EBITDA, a type of operating profit, grew 37%.

What changed? Over the past few years, Innscor has poured money into new factories, new capacity, and new products.

For a while, those decisions were hurting profitability. Now, those same decisions appear to be paying off.

Let’s unpack!

What Innscor’s numbers tell us about Zimbabwe

Before we get into the details, let’s think about what these results mean at a high level.

Innscor makes bread, flour, pork, chicken, snacks, and drinks. Basic consumer goods. People buy them because they need to eat. So when volumes are up 28% in bread, 71% in snacks, 32% in pork, and 33% in pasta, that is broad-based demand.

From a first principles perspective, you do not get that kind of volume growth unless there is more money circulating in the economy.

It may not feel that way, especially if it is not circulating into your pocket. But the trend we are seeing with companies like Delta, Econet, and others is that there is more economic activity than we would think.

So some of what is driving Innscor’s improvement is the environment. But not all of it.

The capital allocation payoff

A business is ultimately the sum total of every capital allocation decision it has ever made. Where, when, and how much you invest shapes a business’s future.

Innscor’s annual capex went from $8 million in 2020 to over $70 million by 2024. New bakery lines. New piggeries. New snack factories. New brewing capacity.

It takes money to make money.

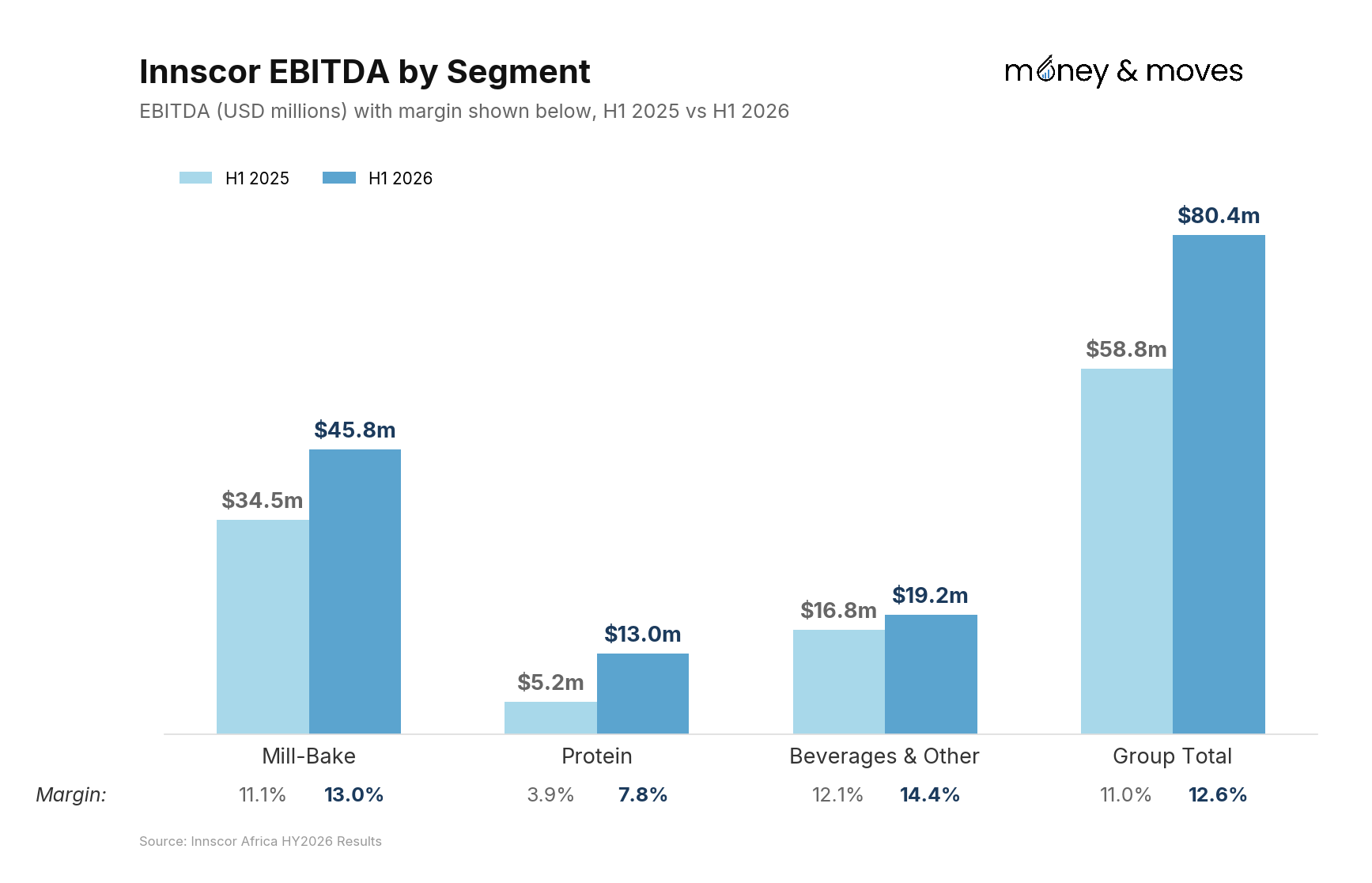

But there is always a gap between spending it and seeing the returns. For Innscor, that gap appears to be closing, with EBITDA rising from $58.8 million to $80.4 million.

The Mill-Bake division, which includes National Foods, the Bakery division, Nutrimaster, and Profeeds, was the biggest contributor, adding $11.3 million of extra EBITDA.

The new automated bakery line in Harare, which was still under construction last time, is now running. Loaf volumes are up 28% with better efficiency. The Snacks division grew 71% on capacity that was already paid for. National Foods’ flour volumes grew 13%.

Yet again, increases in volumes across the board.

Protein was the turnaround story, adding $7.8 million. Two years ago, Innscor invested heavily in its piggeries at Triple C Pigs. That seems to be now delivering results.

Colcom’s volumes jumped 32% (people must have really been braaiing). More product through the same factories means fixed costs spread across more units. The segment’s margin doubled from 3.9% to 7.8%.

This is a big shift from last time, when Colcom’s volumes were actually down 3% after the reclassification of pork from VAT-exempt to standard-rated, which put formal operators at a disadvantage to non-compliant competitors.

Together, these two segments delivered $19 million of the total $21.5 million improvement.

Is this sustainable, and the Tanganda play

There should still be room for improvement.

As mentioned last time, the beverage business is most likely still not operating at full capacity. And with the potential of Tanganda being added to the books, there may be more opportunities ahead.

Innscor recently took up a 27% stake through its subsidiary Rutanhi Beverages, which underwrote Tanganda’s $8 million rights issue.

Now, Tanganda isn’t yet an Innscor subsidiary, but they have already indicated they plan to make an offer to minorities to buy them out. That 27% is like a deposit on a house. You don’t put it down unless you have serious intentions.

That said, Tanganda would be a turnaround case. It had to push for an $8 million rights offer, of which $6.4 million is for working capital.

The good thing is Innscor has always been excellent at generating cash.

If cash were the limiting factor, then Tanganda could get a real boost if Innscor were to go on to own it.

On the other hand, the record of working capital-related rights offers is questionable. Ask OK Zimbabwe and Truworths, who tried before and ended up broke.

However, neither of those companies had a “Big Brother”(a single dominant/controlling shareholder), and there are few better big brothers to have than Innscor.

Where’s the Money? What’s the Move? Is Innscor a good buy right now?

At a market cap of about $750 million and annualised profit of roughly $78.5 million going to shareholders of the parent, Innscor trades on a P/E ratio of about 9.5x. Tiger Brands, a similar business on the JSE, trades at about 11x.

That gap is narrower than you would expect given Zimbabwe’s country risk, although one must also factor in that Innscor is growing much, much faster.

However, we also have to consider that the share price has more than doubled over the past year.

At current levels, it is hard to say Innscor is still cheap. It still seems like a good business, but not as good an investment as it was a year ago when we first mentioned it.

This is also when you consider that Delta is trading at a P/E ratio of about 7-8 when you also annualise their half-year results, and Econet was at about 5-6.

It’s interesting that nearly all the Innscor and Excor businesses (former or affiliated Innscor companies) are trading at a bit of a premium right now.

A final point.

The big 3, Innscor, Econet, and Delta have all posted strong results over the past year.

That points to real economic growth in parts of the Zimbabwean market. But here is the funny thing.

This is also a period where companies filing for corporate rescue have been on the rise, and the confidence in Zimbabwean capital markets is at a low.

This highlights a key insight.

Where you play in the Zimbabwean market is critical. There are seas of opportunities, but there are also deserts.

But wherever you find yourself, one thing doesn't change: it takes money to make money.

Thanks for reading. If you enjoyed this, please share it with someone you know and subscribe for free if you are not already subscribed.

What do you think about Innscor?

P.S. I am working with publicly available information, so I could be wrong or missing something. Thanks for reading!

Another good one Tinashe. I recently discovered a company called Collins Foods in Australia, they run KFCs. It made me realise just how brilliant the Excor gang is. Simbisa is younger than Collins, but has grown it's outlets faster and now pushes more volume.

The only reason it doesn't have same revenue, is because they charge half the prices.

Matching a player in the developed west while playing in Zimbabwe is unheard of in most sectors.

A superb company run by an excellent group of managers led by a genius!