OK Zimbabwe’s Store Closures, Key Takeaways from the G20 Summit: The Week Ahead

A closer look at OK’s shrinking footprint, followed by what the G20 meetings mean for African economies going forward.

This week, we're covering two key stories that you need to watch in the week ahead.

OK Zimbabwe’s Store Closures

G20 Summit: What It Means for Africa — and Why Debt Still Dominates

Let’s unpack.

OK Zimbabwe Closes More Stores – But Is It Enough?

OK Zimbabwe, once the country’s largest retailer, continues to struggle. Last week’s trading update confirmed that “revenue generation remains below break-even levels.”

The update revealed that OK has closed 11 stores deemed “no longer viable,” reducing its footprint to 62 stores. While these closures make sense, the numbers suggest OK may need to close 20+ additional stores to manage its working capital requirements effectively.

The Working Capital Challenge

Back in 2015, when OK was healthy, its net working capital (current assets less current liabilities) stood at $22m.

As at 31 March 2025—the most recent figures available—that position had deteriorated to negative $19m, creating a $41m gap to return to 2015 levels.

OK raised $20m through a rights issue but has struggled to secure the planned $10.5m from property sales. With only the $20m in hand, they have just half of the $41m needed to restore 2015 working capital levels.

Here’s the problem: in 2015, OK operated 61 stores. Today, even after recent closures, it has 62 stores—essentially the same footprint but with half the working capital and significantly weaker credit terms from suppliers.

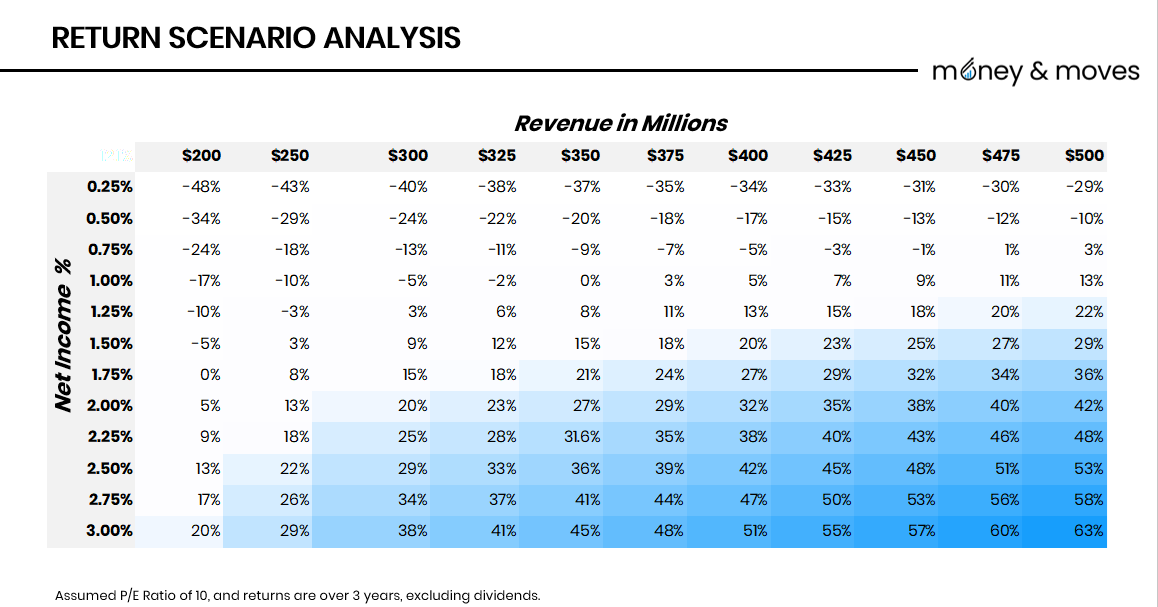

Given these dynamics, sustaining 62 stores appears increasingly challenging. The only realistic option may be cutting another 20+ locations. It’s better to operate 30 well-stocked stores than 60 stores with limited inventory.

This aligns with our analysis during the rights issue, which showed that the best path to favourable returns was to become smaller but more profitable (the numbers in blue in the table. For a more detailed deep dive, you can read the earlier article here)

What Delta’s Results Tell Us

Another revealing data point: Delta generated 92% of its revenue in USD over the last half year. Since large formal chains still conduct significant trading in ZiG, Delta’s results indirectly suggest that major retail chains like OK are no longer as important a sales channel.

OK was once a big draw for suppliers—a must-have relationship. That appears to have changed.

G20 Summit: What It Means for Africa — and Why Debt Still Dominates

This past weekend’s G20 summit in South Africa marked a historic first: Africa hosting the world’s premier economic forum.

The G20 comprises 19 countries plus the European Union and African Union, representing 85% of global GDP, 75% of world trade, and two-thirds of humanity.

Think of it as the board of directors for the global economy—setting direction on interest rates, tax policy, climate finance, and banking regulations.

Africa’s Critical Challenge: Debt

In my view, the most significant topic for Africa was still the debt-dominated discussions.

Across the continent, governments are spending huge portions of revenue simply servicing old loans, creating a hidden tax that strangles entire economies and hits businesses hardest.

Here’s what high debt service means on the ground:

Taxes rise relentlessly — VAT, fuel levies, PAYE, corporate rates all climb to meet obligations

Credit ratings fall, making new borrowing even more expensive, worsening the trap

Chronic deficits emerge — governments borrow again just to repay old debt

This vicious cycle is trapping economies across the continent.

Kenya’s controversial 2024 Finance Bill—which triggered deadly protests—was about raising revenue, which was also in large part for payments.

As of May 2025, Kenya spends 67.1% of its revenue on debt service. When two-thirds of income goes to paying for old loans, governments either raise taxes, borrow more, or cut services.

Zimbabwe’s crisis is even graver. External debt service equals 119.5% of government revenue—meaning even using all revenue wouldn’t cover what’s owed. Zimbabwe’s debt also includes areas, and the $3.25 billion owed to former commercial farmers for farm improvements.

Who’s Responsible?

African governments share responsibility through off-budget borrowing, unsustainable subsidies, weak fiscal discipline, and political spending.

But systemic shocks matter too: COVID devastated tourism and exports, rising global rates increased borrowing costs, and geopolitical tensions complicated debt negotiations. Crucially, countries shouldn’t pay indefinitely for past administrations’ mistakes.

Part of the reason why capital is so expensive is because of this debt overhang that hits Africa the hardest.

Progress on debt restructuring remains slow because real solutions require IMF consensus, and the US, the notable absentee from the summit, has veto power.

It also doesn't help that China and Western creditors disagree on restructuring terms, and many African governments lack fiscal transparency.

The symbolism of this weekend’s summit was powerful, but structural debt problems aren’t going away.

Still, visibility matters. The summit brought Africa closer to the centre of global economic conversations than ever before.

It also allowed Cyril Ramaphosa to flex a bit at the US, or as the white house press secretary put it, run his mouth:

“I saw the South African president running his mouth a little bit against the United States and the president of the United States earlier today, and that language is not appreciated by the president or his team.”- White House press secretary, Karoline Leavitt

I can imagine Cyril saying to himself, “Trump, keep your USA, and I’ll keep my South Africa”.