Will Starlink Disrupt Liquid's Business? The Battle for Africa’s Internet Market

Last week, we discussed how Starlink would impact Econet’s mobile network business.

Today, we will examine the impact of Starlink on Econet’s sister company, Liquid Intelligent Technologies (Liquid), which is in the internet infrastructure business.

Firstly, to understand the impact Starlink may have, we need to understand how Liquid makes money.

The best source of this information is Liquid’s Offering Memorandum from 2021.

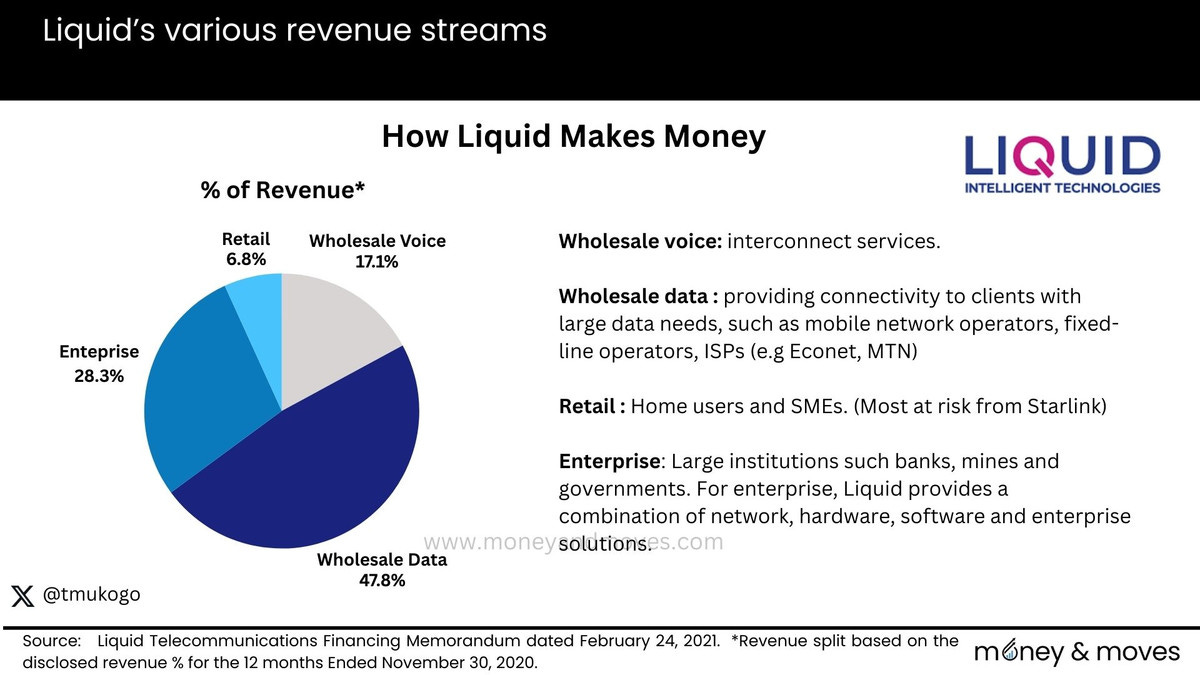

From this, we see that Liquid’s revenue split was as follows:

Wholesale Voice 17.1% (interconnect services)

Wholesale Data 47.8%

Enterprise 28.3% (large organisations)

Retail (consumers and SMEs) 6.8%.

When you look at each business segment’s contribution to revenue, it’s clear why Liquid may feel Starlink’s entry won't affect their business too much.

The primary revenue at risk from Starlink comes from the Retail side, which accounts for only 6.8% of total revenue.

The retail business provides internet to households and small and medium businesses, which are the segments that seem to be buying Starlink the most.

Now, for Zimbabwe specifically, I think the risk is greater than for the rest of the Liquid group overall.

Firstly, the 6.8% contribution of Retail to the group revenue is distorted by South Africa, which has the highest revenue but doesn’t have a retail business.

When we adjust for this, Retail's contribution to total revenue is 12.4%. Given that Liquid is the market leader in Zimbabwe, Retail's revenue contribution is likely to be higher than 12.4%.

Based on my estimates, the Retail business in Zimbabwe accounts for 15% to 25% of total revenue, Enterprise for 25% to 35%, and Wholesale for 45% to 55%.

These figures are derived from the offering memorandum and adjusted for specifics related to Zimbabwe.

Now, on the Wholesale Data side in Zimbabwe, Liquid seems pretty safe.

Their biggest customer is Econet Wireless, which will obviously not change. That means about half of Liquid's revenue has limited risks from Starlink.

Currently, the risk on the Enterprise side seems low. Enterprise clients include large institutions, banks, mines, etc. Liquid offers a blend of network, hardware, software, and enterprise solutions for these customers that Starlink doesn't directly replace.

However, Liquid must be careful about technological solutions that could change this dynamic. CFOs are always looking to cut costs.

If a technological solution is found that can effectively leverage Starlink for these purposes, it could quickly scale once it proves successful with just one enterprise customer.

This already means that about 75% to 85% of Liquids' revenue is not primarily at risk from Starlink - for now. However, the Zimbabwe business generated $126 million in revenue, so even if 20% of revenue at risk is still $25 million. That's a lot of revenue you don't want to lose.

To see how much market share Starlink could gain in the next year or two, we can use Nigeria as a case study.

Starlink first launched in Nigeria on February 1, 2023, and by the end of the year was the third-largest ISP with 9% of the market.

While that is impressive, the uptake in Zimbabwe could be even greater since the cost of internet in Zimbabwe is higher than in Nigeria.

If Starlink gained a 9% market share in a year in Nigeria, that number could be 15% in Zimbabwe.

Now, a lot of this growth may not necessarily be people switching from Liquid to Starlink, but to simplify things, let's assume that of Starlink's 15% market share, half is coming from consumers switching to Starlink, and the balance is new customers.

If this is the case, I estimate that Liquid's revenue could fall between $4 million and $8 million over the next year or two due to Starlink.

This is a big number, but there is some buffer for a business that generates $126 million in annual revenue, provided the Enterprise business doesn't suffer any shocks.

However, the most significant impact on Liquid may not be the short-term revenue loss but the margin compression.

Starlink has effectively introduced a price ceiling on the cost of the internet, which will impact Liquid.

However, as we discussed before, Liquid seemed to have quite a bit of buffer in their pricing, which we estimated to be about 45%.

In closing, Starlink will impact Liquid's business but not much on a group level.

Within Zimbabwe, Liquid will likely lose much of its current and future retail business.

However, as long as the enterprise offering is defended, Liquid may still be able to weather the Starlink storm.

Where’s the Money, What’s the Move?

The number of people who have access to high-speed internet will significantly increase over the next year.

If there is one picture that tells this story, it’s this picture of a Starlink on top of a cabin somewhere in Zimbabwe.

This could make online-based businesses more attractive as time spent on the Internet increases.

Linked to this is a potentially higher return on investment in internet-based advertising compared to traditional media avenues.

What do you think? Thanks for reading!

Did you enjoy what you just read? There are +2,500 like-minded people reading Money & Moves every week. Become a Money & Moves partner and sponsor a post. Reply to this email to find out more!

In Case You Missed It: Related posts from the archive to consider checking out:

Does Starlink Mean the End of Econet?

Are Internet Providers in Zimbabwe Overcharging You?

PS: I am working with public information so I could be missing something or simply wrong in my analysis

I loved the breakdown (as always!). Thanks for bringing data into the conversation.

IMO, margin compression looks like the biggest medium to long-term risk for Liquid. It will impact how they handle current debt obligations and approach any future leverage efforts. It's also a significant concern for all Zimbabwean entities that face substantial hurdles in securing capital. You've already articulated in previous articles how the telecoms model is partly built on infrastructure-related capex.

Liquid and EWZ have been good at this and, as such, are the most exposed. They've built part of their competitive advantage around this. But, it won't matter now when it's stacked up against LEO tech which leapfrogs all of this.

RE the enterprise segment - Liquid will have to do a lot of work to endear themselves to their clients. Wouldn't be surprised if SLAs are coming under review. Like you said - CFOs are all about cost-cutting and the noise that Starlink has made feeds into that. Everyone else who provides enterprise services who was outpaced by guys like Liquid could, to some degree, consider the playing field as slightly evened, for now.